ECON101 Lecture Notes - Lecture 14: Vale Limited, Joseph Schumpeter, De Beers

11 Nov 2017

School

Department

Course

Professor

99

ECON101 Full Course Notes

Verified Note

99 documents

Document Summary

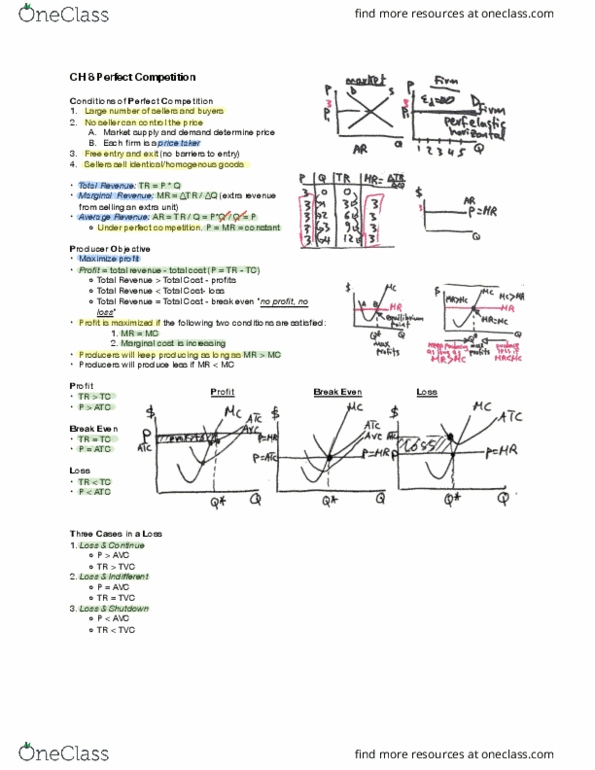

Market supply curve: deri(cid:448)ed (cid:271)(cid:455) horizo(cid:374)tall(cid:455) su(cid:373)(cid:373)i(cid:374)g the i(cid:374)di(cid:448)idual fir(cid:373)"s suppl(cid:455) (cid:272)ur(cid:448)es. Exceptions: (1) weakest link goods (2) best shot goods (1) q=(cid:373)i(cid:374) (cid:894)(cid:395)(cid:1005),(cid:395)(cid:1006), ,(cid:395)(cid:374)(cid:895) (2) q=(cid:373)ax(cid:894)(cid:395)(cid:1005),(cid:395)(cid:1006), ,(cid:395)(cid:374)(cid:895) Long run equilibrium in a perfectly competitive market. In the long run, all costs are variable. In the long run, firms can enter the market and firms can exit the market. (image) In the long run, pi>0 induce entry of new firms. In the long run, pi < 0 induce exit of firms. Exit continues until pi=0: s*, d, p*, q*, d*, q*, pi=0. In a perfectly competitive market, the long run equilibrium occurs at the quantity where tt=0. Or where p=mc and p=atc or where mc=atc: suppose demand increases to d1, short run s0, d1, p1, q1, d1, q1, pi1 > 0, long run pi1>0 induce entry supply increases until pi = 0 until . Pi = r accounting cost; opportunity costs. Economic costs = accounting costs + opportunity costs.