ECON101 Lecture Notes - Lecture 13: Market Power, Marginal Revenue, Marginal Cost

17 Apr 2015

School

Department

Course

Professor

99

ECON101 Full Course Notes

Verified Note

99 documents

Document Summary

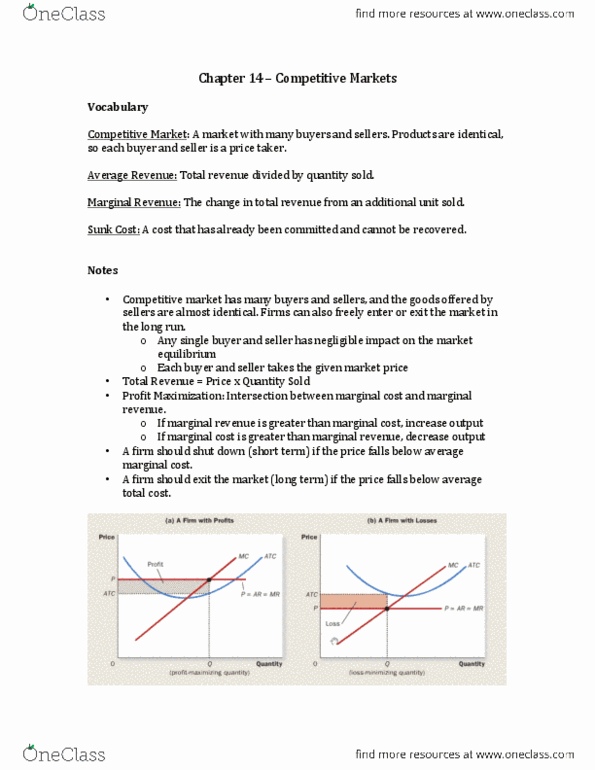

Profit maximization and the competitive firm"s supply curve. Clinton richardson: for a competitive firm, the firm"s price equals both its average and marginal revenue, general rules for profit maximization: If marginal revenue is greater than marginal cost, the firm should increase its output. If marginal cost is greater than marginal revenue, the firm should decrease its output: at the profit-maximizing level of output, marginal revenue and marginal cost are exactly equal. In essence, because the firm"s marginal-cost curve determines the quantity of the good the firm is willing to supply at any price, it is the competitive firm"s supply curve. Spilt milk and other sunk costs: sunk cost a cost that has already been committed and cannot be recovered. The firm"s long-run decision to exit or enter a market: the firm exits the market if the revenue it would get from producing is less than its total costs, exit if tratc.