ECO 1104 Lecture Notes - Lecture 14: Takers, Opportunity Cost, Perfect Competition

31 Jul 2018

School

Department

Course

Professor

16

ECO 1104 Full Course Notes

Verified Note

16 documents

Document Summary

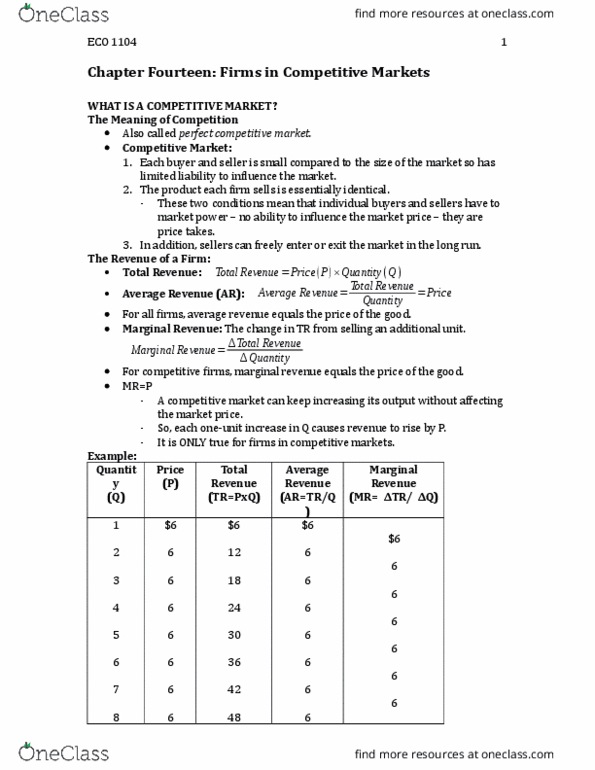

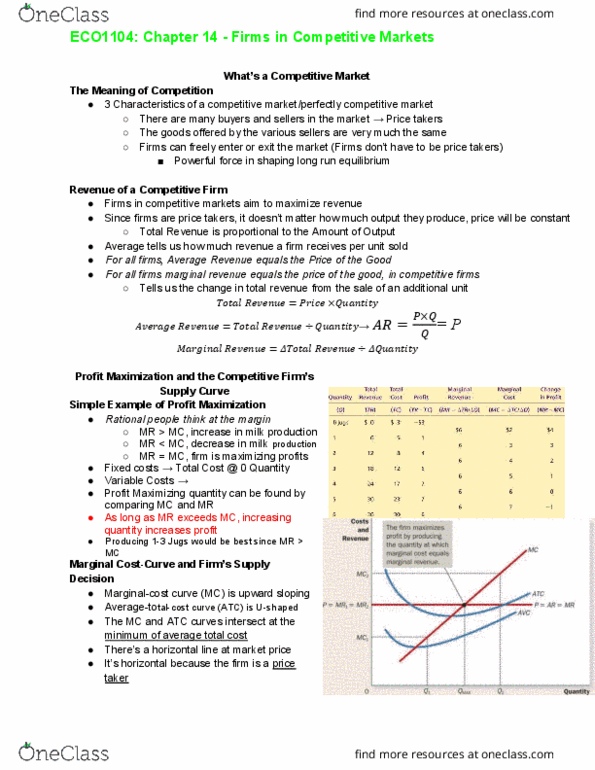

Profit maximization: what quantity maximizes the firm"s profit, to find the answer, think at the margin. If the firm increases quantity by one unit, revenue rises by the marginal revenue and cost rises by the marginal cost. If mr > mc, then profit-maximizing firm will increase quantity to raise profit. If mr < mc, then a profit-maximizing firm will reduce quantity to raise profit. A new firm"s decision to enter market: similarly, a prospective entrant compares the benefits of entering the market (tr) with the costs (tc), and enters if the benefits exceed the costs. Measuring profit: profit = tr tc, profit = (tr/q tc/q) x q, profit = (p atc) x q. Market supply: assumptions: all existing firms and potential entrants have identical costs (firms). The long run: market supply with entry and exit. In the long run, the number of firms can change due to entry and exit.