ECO101H1 Lecture Notes - Organic Food, Marginal Revenue, Fixed Cost

ECO101H1 Full Course Notes

Document Summary

Get access

Related textbook solutions

Related Documents

Related Questions

11)

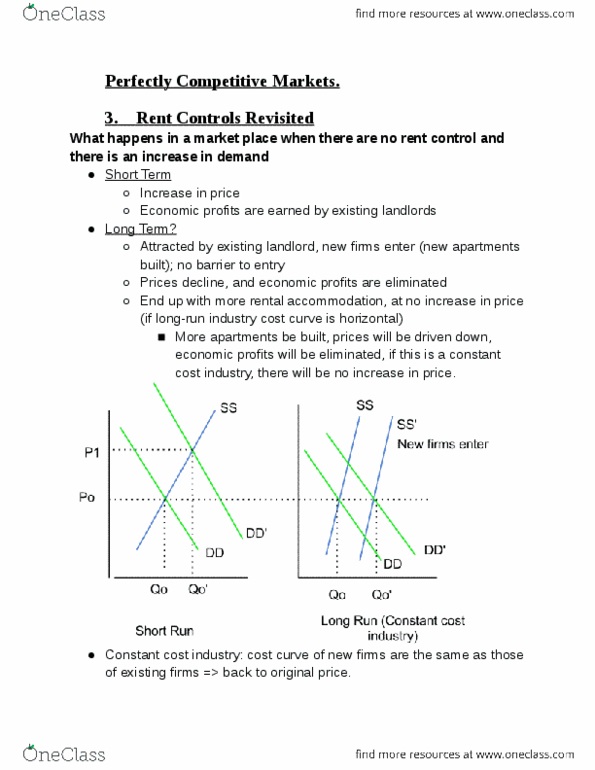

A constant-cost, perfectly competitive industry experiences a permanent increase in demand. In adjusting to this change, what will happen to the price of the product?

|

It will increase in the short-run and then decrease in the long-run, but end up above its original level in the long-run. |

|

|

It will increase in the short-run and then increase further in the long-run. |

|

|

It will increase in the short-run and then decrease back to its original level in the long-run. |

|

|

It will increase in the short-run and then decrease below its original level in the long-run. |

|

|

It will decrease in the short-run but return to its original level in the long-run. |

12)

Assume that a perfectly competitive firm owns or rents a higher-quality resource that results in lower average total costs and higher economic profits in the short run. What will happen in the long-run?

|

The price of the higher-quality resource will be bid upward resulting in economic rents and equalizing costs across firms. |

|

|

New firms will enter and compete with any excess profits away. |

|

|

None of the other answers is correct. |

|

|

The government will tax away any excess profits. |

|

|

The firm with the higher-quality resource will earn positive economic profits in the long run. |

13)

Which of the following are characteristics of long-run equilibrium?

|

No firm has an incentive to change its level of output. |

|

|

No firm has an incentive to change its plant size. |

|

|

Economic profit is zero |

|

|

All of the above |

|

|

None of the above |

14)

Which of the following statements is consistent with the textbookâs analysis of perfect competition?

|

Although individual perfectly competitive firms wonât pay to advertise, the industry as a whole may well advertise. |

|

|

Higher costs for one firm in the industry will result in that firm charging a higher price than the other firms in the industry. |

|

|

If all the firms in an industry charge an identical price for their products, this is clear evidence of collusive behavior. |

|

|

All of the above |

|

|

None of the above |

15)

The assumptions that define the market structure known as monopoly include which of the following?

|

High barriers to entry. |

|

|

There is one seller. |

|

|

There are no close substitutes available. |

|

|

All of the above |

|

|

None of the above |