ECO100Y1 Lecture Notes - Lecture 8: Marginal Revenue, Perfect Competition, Demand Curve

Document Summary

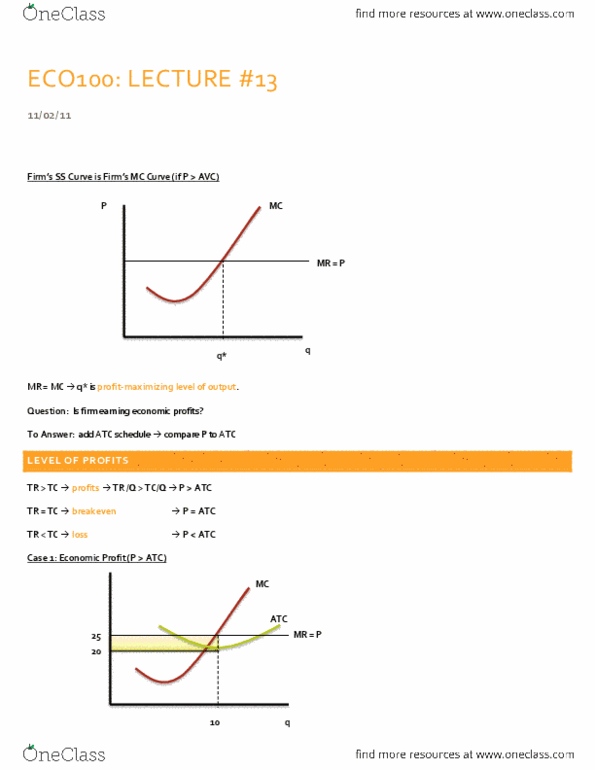

Total revenue, average revenue, marginal revenue for perfectly competitive firm: example. Q p tr (p*q) ar (tr/q) mr (cid:894) tr/ q(cid:895) Marginal revenue: the change in total revenue from an additional unit sold. Average revenue: total revenue divided by the quantity sold. Profit maximization: insight: firms are price takers (cannot influence price, must choose level of output that maximizes profits, given market price. At q2(q0): mr=mc profit-maximizing output (do not change output) To find the profit-maximizing le(cid:448)el of output (cid:894)(cid:395)(cid:895), the only cost schedule (cid:449)e (cid:374)eed is the fi(cid:396)(cid:373)"s mc schedule. [the only variable a perfectly competitive firm can change is its output, not price, because it has a perfectly elastic demand curve. Consumers are willing to buy unlimited amount of products at a fixed (market) price, but quantity will be zero if the price changes, therefore, revenue will fall to zero. ] If price is ____, firm will supply ____.