ECO204Y1 Lecture Notes - Lecture 4: Indifference Curve, Utility Maximization Problem, Convex Preferences

Document Summary

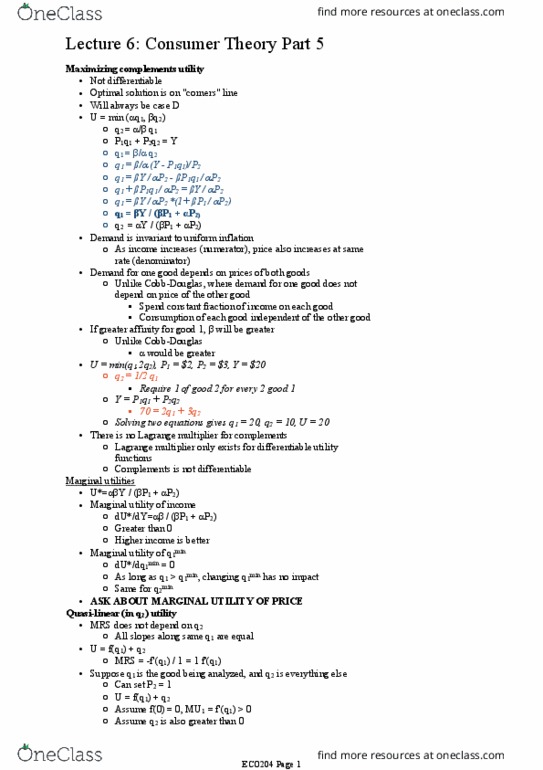

Rescale so that + = 1. U = min( q1, q2) where , > 0. / of good 2 for every unit of good 1. Units of good 2 for units of good 1. Suppose f(q1) = -1/2 q1 q1 = portfolio risk (standard deviation of returns) q2 = portfolio return (average returns) U = -1/2 (portfolio risk)2 + portfolio return. Mrs = -mu1 / mu2 = portfolio risk. As portfolio risk increases, portfolio return must increase even more. Greater levels of returns required as risk increases. Set of affordable bundles p1q1 + p2q2 = y. Budget line: q2 = y/p2 - p1/p2 q1. No change in set of affordable bundles if all pecuniary parameters increase by same percentage. Assume rational preferences, all pecuniary parameters strictly positive. For two goods with strictly convex preferences and smooth indifference curves max u (q1,q2) s. t. p1q1 + p2q2 = y, q1 >/= 0, q2 >/= 0.