RSM423H1 Lecture 8: Lecture 8

Document Summary

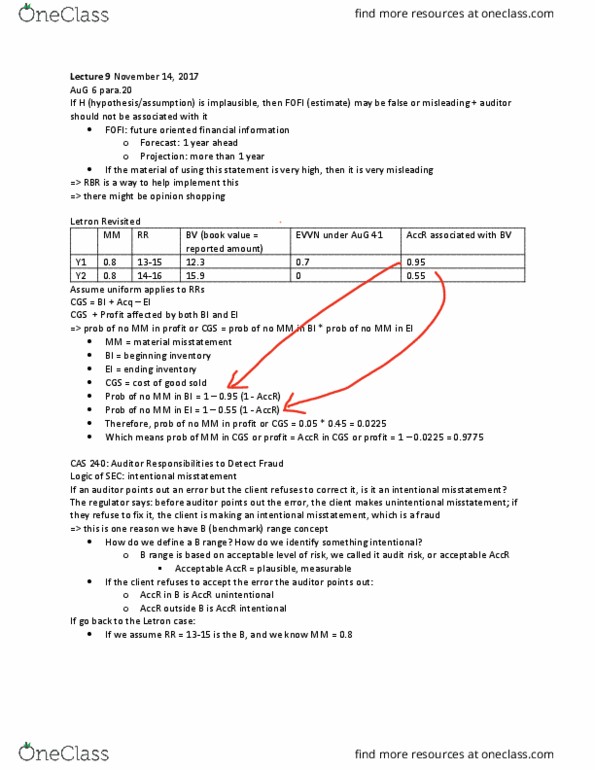

If significant risks (aka not acceptable risks) exist for an estimation uncertainty, then client may need to switch to a different reporting framework (such as going concern assumption) In order to reduce the legitimate range, we should get more evidence. => cas 40 a49: the above might not be possible. Chapter 19 part ii pp14-15 class 6-8 ln. Sec detailed rules must be followed (conceptual framework at bottom: verifiability required, past transactions required, order of concepts is important (objective at top) Aug-6 audits of fofi (future oriented financial information) If a hypothesis in projection is not plausible (unacceptable accr) in the circumstances then the info may be false or misleading and the cpa will be prohibited by rules of professional conduct from being associated with it. Let"s (cid:272)al(cid:272)ulate a(cid:272)(cid:272)r assu(cid:373)i(cid:374)g u(cid:374)ifor(cid:373) distri(cid:271)utio(cid:374) (ho(cid:449) (cid:373)u(cid:272)h assura(cid:374)(cid:272)e if (cid:449)e assu(cid:373)i(cid:374)g u(cid:374)ifor(cid:373) distribution?) If you record 13 for y1, accr = (15-13. 8)/(15-13)=1. 2/2=0. 6 [13. 8=13+0. 8]