RSM423H1 Lecture Notes - Lecture 9: Audit Risk, Financial Statement, Mci Inc.

Document Summary

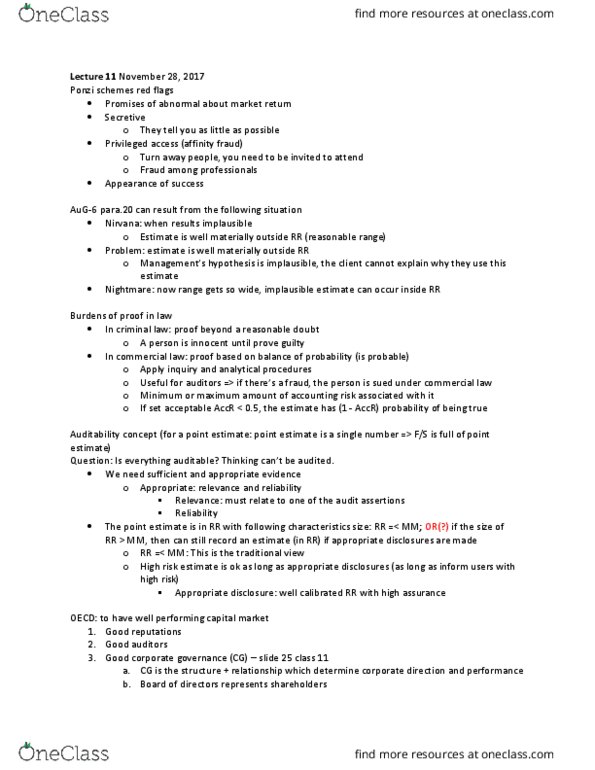

If h (hypothesis/assumption) is implausible, then fofi (estimate) may be false or misleading + auditor should not be associated with it: fofi: future oriented financial information, forecast: 1 year ahead, projection: more than 1 year. If the material of using this statement is very high, then it is very misleading. => rbr is a way to help implement this. Cgs + profit affected by both bi and ei. The regulator says: before auditor points out the error, the client makes unintentional misstatement; if they refuse to fix it, the client is making an intentional misstatement, which is a fraud. How do we identify something intentional: b range is based on acceptable level of risk, we called it audit risk, or acceptable accr, acceptable accr = plausible, measurable. If the client refuses to accept the error the auditor points out: accr in b is accr unintentional, accr outside b is accr intentional.