Economics 1021A/B Lecture Notes - Economic Surplus, Demand Curve, Externality

1 Dec 2012

School

Department

Course

Professor

94

ECON 1021A/B Full Course Notes

Verified Note

94 documents

Document Summary

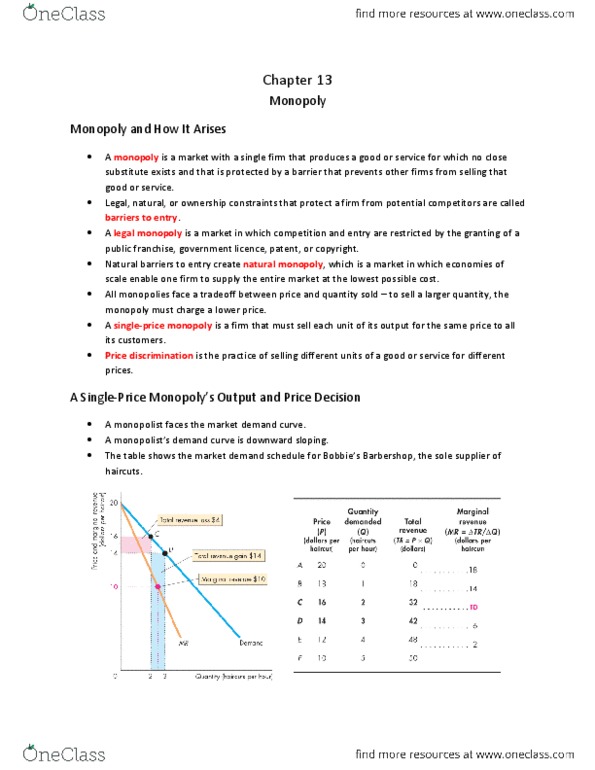

Topic 10: monopoly: introduction, possible sr equilibrium, possible lr equilibrium, dead-weight loss and question of efficiency, conclusion, introduction. We really like perfect competition, but nothing"s perfect so we"re looking at the exact opposite: one seller, homogenous product - you have no choice, very difficult entry. *control of scarce resources (gold only in a few countries, etc. ) Monopolists to do have a perfectly elastic demand curve (horizontal). They are both the firm and the industry so the market is a profit maximizing entity. Any firm has to follow the criteria in topic 6, so monopoly will follow that too: possible sr equilibrium. There are three possible short run equilibria for the monopolist. One in which the monopolist earns positive economic profits, one in which it earns zero economic profits and one in which is negative. In the latter case, the firm may or may not operate. Go up from there to ac that"s the cost to run at q*.