BU127 Lecture Notes - Lecture 4: Cash Flow, Asset, Deferred Income

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

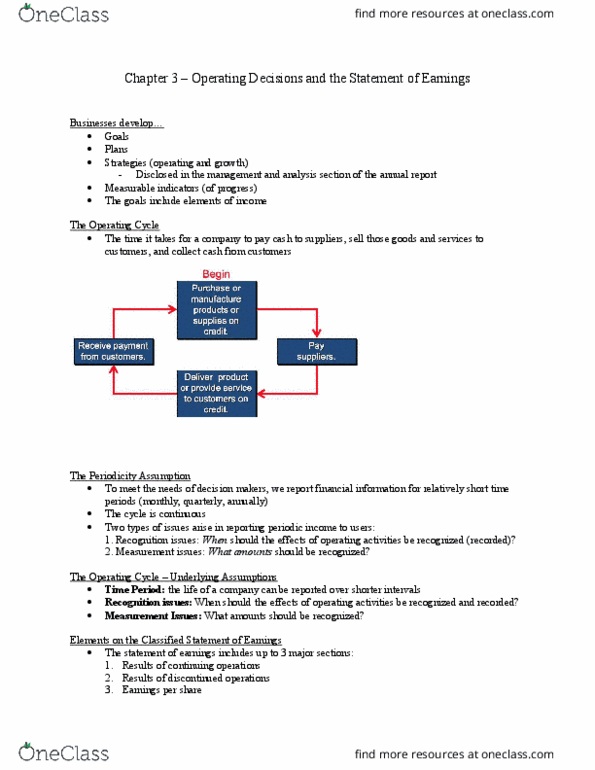

The periodicity assumption: to meet the needs of decision makers, we report financial information for relatively short time period (monthly, quarterly, annualy) Time period: the long life of a company can be reported over a series of shorter time periods. Cash flow important have enough to pay suppliers. Pay suppliers: results of continuing operations, results of discontinued operations, earnings per share. Results of continuing operations; two formats: single step, multiple step cost of goods sold deducted from sales to present gross margin as a subtotal. Other operating expenses then deducted to show operating earnings as second subtotal do this one, put lots of subheadings in. Discontinued operations: result from the disposal of a major segment of the business and are reported net of the related income tax effects. The entity has transferred to the buyer the significant risks and rewards of ownership. The entity retains neither continuing managerial involvement nor effective control over the goods sold.