BU247 Lecture Notes - Lecture 7: Fixed Cost, Capacity Utilization

Document Summary

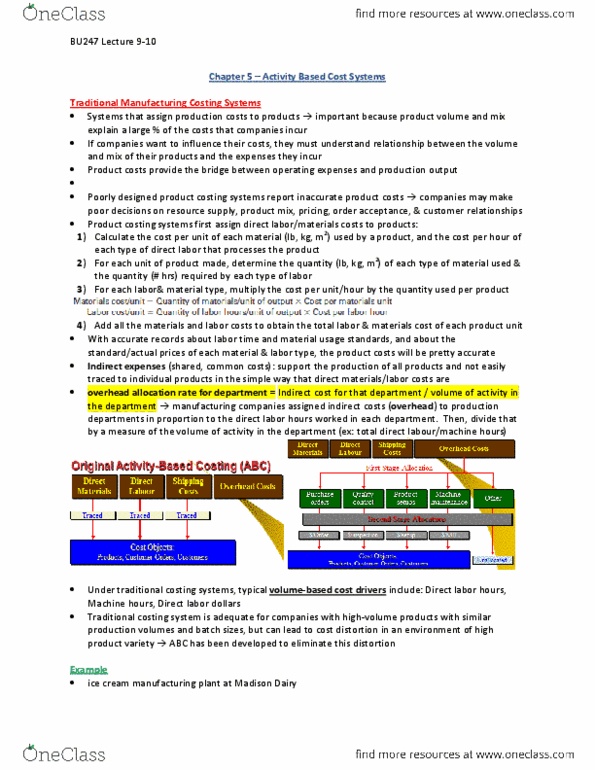

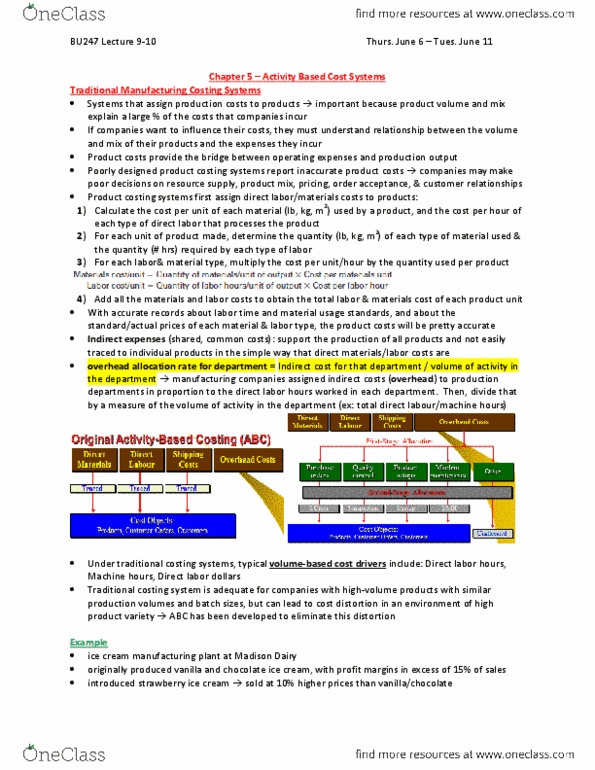

Product costing systems are important because product volume and mix explain a large percentage of the costs that companies incur. Product costs provide the bridge between operating expenses and production output. If poorly designed product costing systems report inaccurate product costs, companies can make poor decisions on resource supply, product mix, pricing, order acceptance, and customer relationships. Product costing systems start by assigning direct labour and direct materials cost to products. Calculate cost per unit of each material used by a product and the cost per hour of each type of direct labour that processes the product. For each unit of product made, determine quantity of each type of material used and quantity required for each type of labour. For each labour and material type, multiply the cost per unit by quantities used per product: materials cost/unit = quantity of materials/units of output x. Cost per materials unit: labour cost/unit = quantity of labour hours/units of output x.