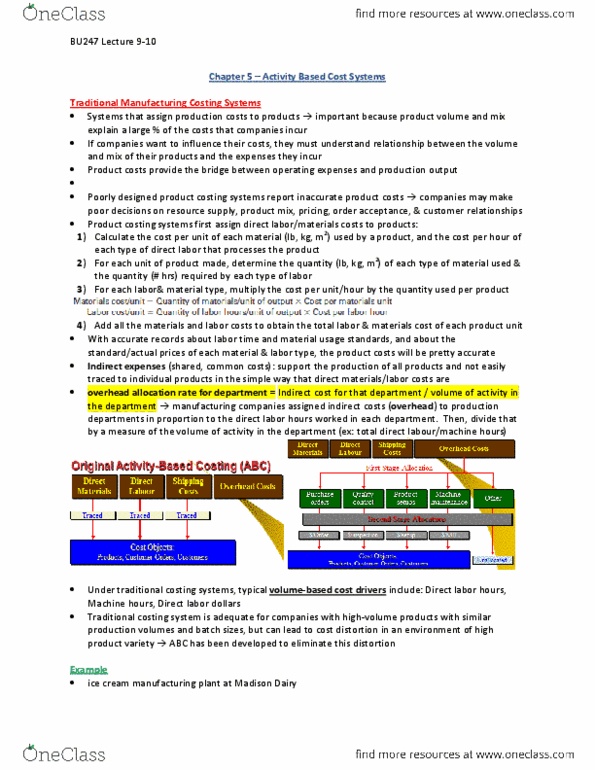

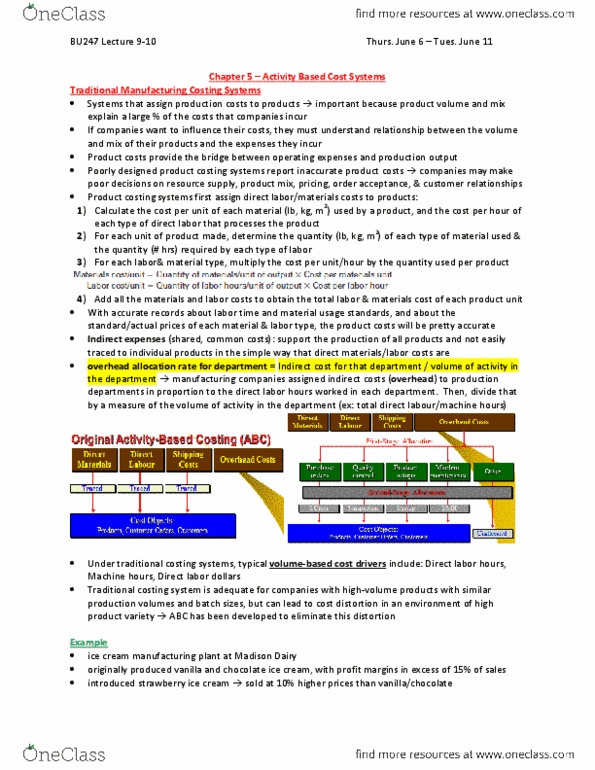

BU247 Lecture Notes - Lecture 4: Indirect Costs, Session 9, Cost Driver

Document Summary

Capacity = capacity can be used as the total volume of the cost driver 1. Theoretical capacity = 1000 hours (maintenance brings it down: practical capacity = 900 hours (most used and stable, planned capacity = 800 hours, average capacity = 850 hours. Allocated vs incurred = difference between actual (incurred) and applied (allocated) = cost of idle capacity. Cash flow in organizations: manufacturing organizations = summarizes the manufacturing sequence in a simple organization. Classified into three groups: direct materials, direct labor, and manufacturing overhead. Direct materials work in process (direct labor and manufacturing overhead) finished goods. Inventory cost of goods sold: retail organizations = summarizes the flow of activities in a retail organization. Inventory (overhead items) cost of merchandise sold: service organizations = summarizes the flow of activities, such as a consultancy, that undertakes major projects. Session 9 (the nature of indirect (overhead) costs.