BU487 Lecture Notes - Lecture 7: Retained Earnings, Accounts Receivable, Independent Business

Document Summary

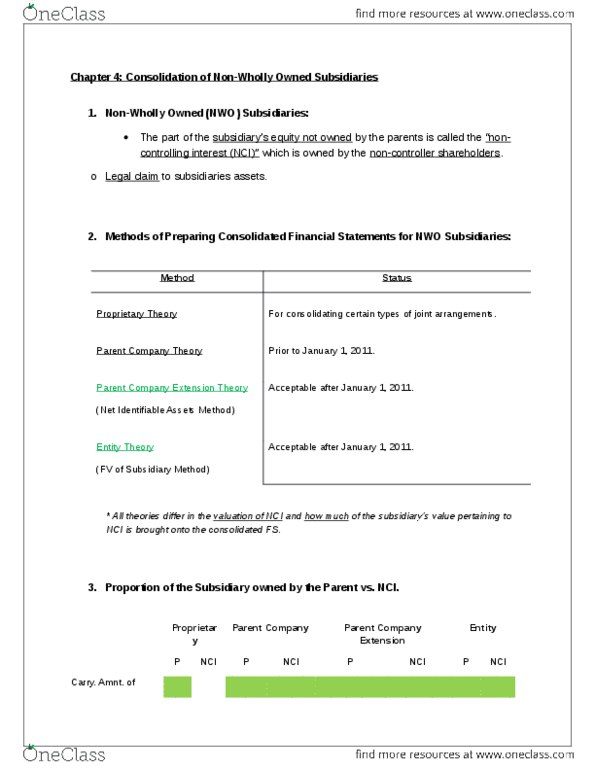

Introduction to consolidation theories: four theories propose a solution to preparing consolidated financial. Statements for non-wholly owned subsidiaries: proprietary theory, parent company theory, parent company extension theory, entity theory, old: parent company theory was used in canada before january 1, 2011. Proprietary theory is presently used for consolidating certain types of joint arrangements and was an option under gaap prior to 2013 for consolidating joint ventures: new: on january 1, 2011 the entity theory replaced parent company. Theory as an acceptable method of consolidating subsidiaries: option: the parent company extension theory is also acceptable after. January 1, 2011 or sooner: compare the four theories, you can see differences in the followings: Implied fair value= value of the shares acquired. + estimated value of shares not acquired: the entity theory- estimated value of shares not acquired, three ways: If there is no market price for the subsidiary, use the price paid by the.