BU487 Chapter Notes - Chapter 4: Book Value, Sub Sub, Equity Method

Document Summary

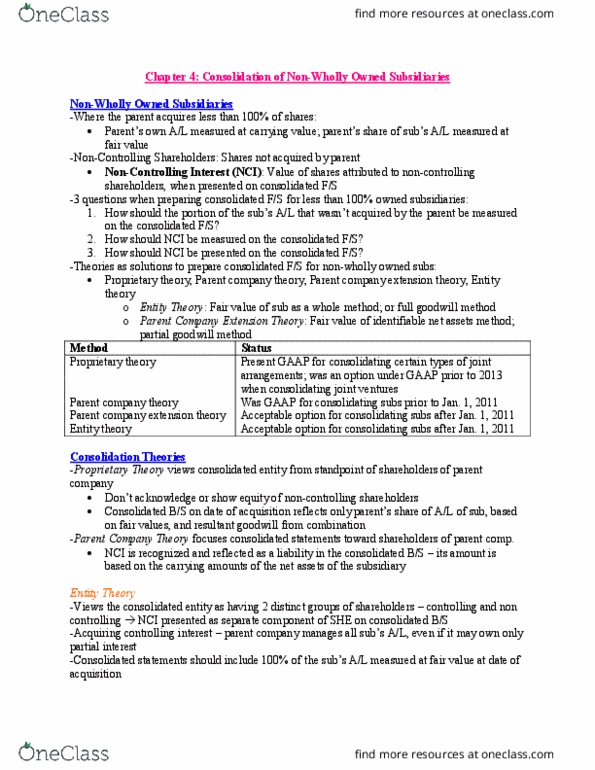

Acceptable after january 1, 2011. (net identifiable assets method) Acceptable after january 1, 2011. (fv of subsidiary method) * all theories differ in the valuation of nci and how much of the subsidiary"s value pertaining to. Nci is brought onto the consolidated fs: proportion of the subsidiary owned by the parent vs. nci. * the parent"s portion of the subsidiary"s value is fully represented under all theories. The nci"s share varies under the four theories. Note: goodwill (except in the entity theory where the entire implied balance is included) and. Not always proportional: much higher goodwill for the parent if a premium is paid. Invented to address the concerns of goodwill evaluation under entity theory: values both the parent"s share and the nci"s share of identifiable net assets at. Paren (parent share of ownership * fv of. [parent share of ownership * (fv sub carrying amount of sub)] Fv of sub + (parent share of ownership *