ACTG 2010 Lecture Notes - Lecture 8: Balanced Scorecard, Takeover Target, Intangible Asset

28 Aug 2016

School

Department

Course

Professor

Document Summary

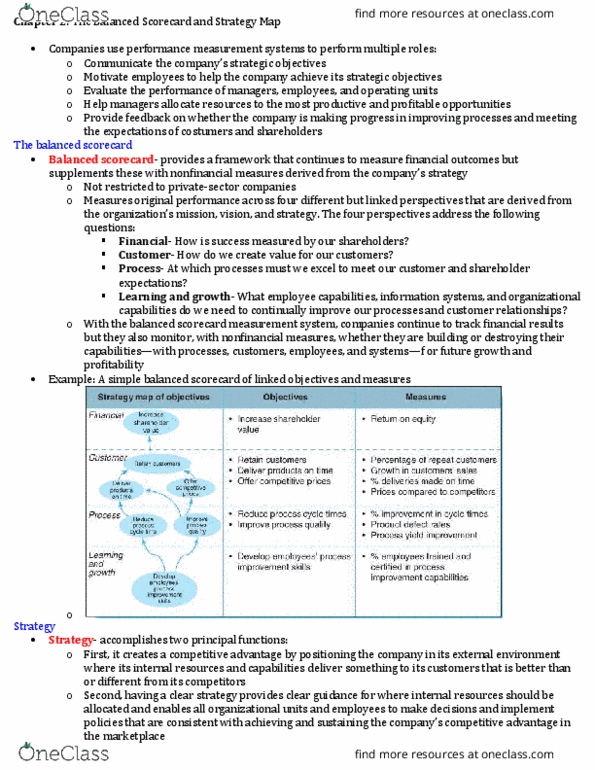

Traditional financial performance metrics provide information about a firm"s past results, but are not well-suited for predicting future performance or for implementing and controlling the firm"s strategic plan. By analyzing perspectives other than the financial one, managers can better translate the organization"s strategy into actionable objectives and better measure how well the strategic plan is executing. The balanced scorecard is a management system that maps an organization"s strategic objectives into performance metrics in four perspectives: financial, internal processes, customers, and learning and growth. These perspectives provide relevant feedback as to how well the strategic plan is executing so that adjustments can be made as necessary. The balance scorecard framework can be depicted as follows: The balanced scorecard (bsc) was published in 1992 by robert kaplan and david. In addition to measuring current performance in financial terms, the balanced. Scorecard evaluates the firm"s efforts for future improvement using process, customer, and learning and growth metrics.