ACCT1022 Lecture Notes - Lecture 6: Net Income

16 Feb 2017

School

Department

Course

Professor

Document Summary

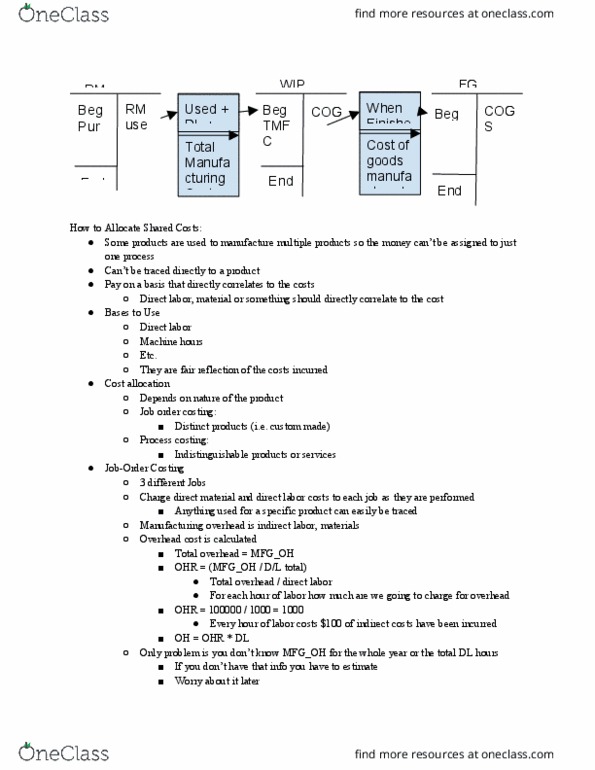

Say the total overhead for the year is denoted mfg_oh and allocation is made based on direct labor hours. Say the total direct labor hours that will be consumed by all jobs in the year is denoted dltotal. Then the rate at which you allocate overhead is the overhead rate: ohr = mfg_oh/dltotal. If dlcrates = the direct labor hours consumed by the crates job, then: overhead allocated to the crates job ohcrates = ohr *dlcrates. What is the catch: exact dollar amount of mfg_oh for the period is not known, neither is dl total. Thus, companies work with the predetermined overhead rates (pohrs) The predetermined overhead rate (pohr) used to apply overhead to jobs is determined before the period begins. Pohr = estimated total manufacturing overhead cost for the coming period/estimated total units in the allocation base for the coming period. The predetermined overhead rate (pohr) used to apply overhead to jobs as determined before the period begins.