SMG AC 222 Lecture Notes - Lecture 5: Earnings Before Interest And Taxes, Fixed Cost, Variable Cost

28 Jul 2016

School

Department

Course

Professor

Document Summary

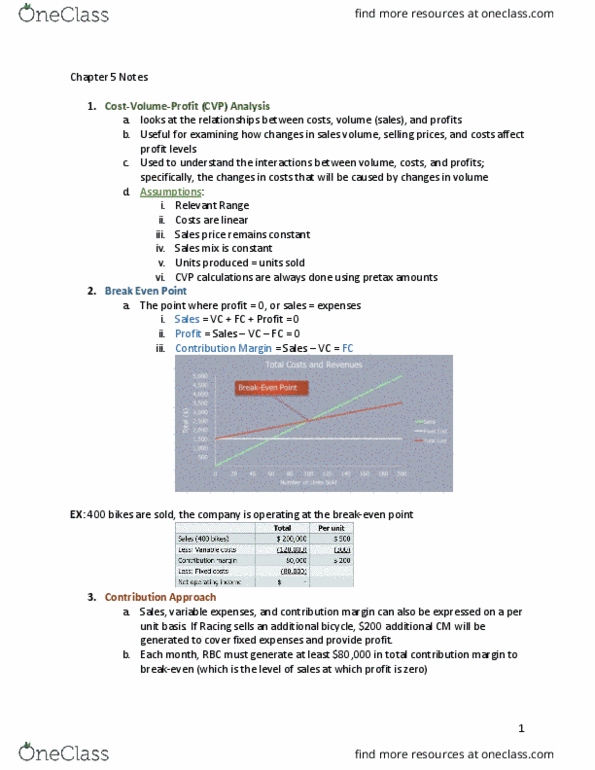

Chapter 5: key assumptions of cost-volume-profit analysis. Variable cost constant per unit and total fixed cost constant: calculate break-even point (in units and in sales) Profit = (selling price per unit variable cost per unit) * units produced fixed expenses. B-e in sales dollars = fixed expenses / contribution margin ratio. Contribution margin ratio = contribution margin / sales (used to quickly determine if an increase of sales, how much will the net operating income will increase: calculate with a target profit. Units needed = (target profit + fixed expenses) / contribution margin. Sales dollars needed = (target profit + fixed expenses) / contribution margin ratio: cvp graph, calculate margin of safety. Margin of safety in dollars= total sales break-even sales. Margin of safety in units = units produced. Advantage: in good years, because fixed cost enlarges the factory"s production capability, the manufactory will earn more profit than factory with small fixed expenses.