ACC 208 Lecture Notes - Lecture 14: Earnings Before Interest And Taxes, Contribution Margin, Operating Leverage

15 Dec 2016

School

Department

Course

Professor

Document Summary

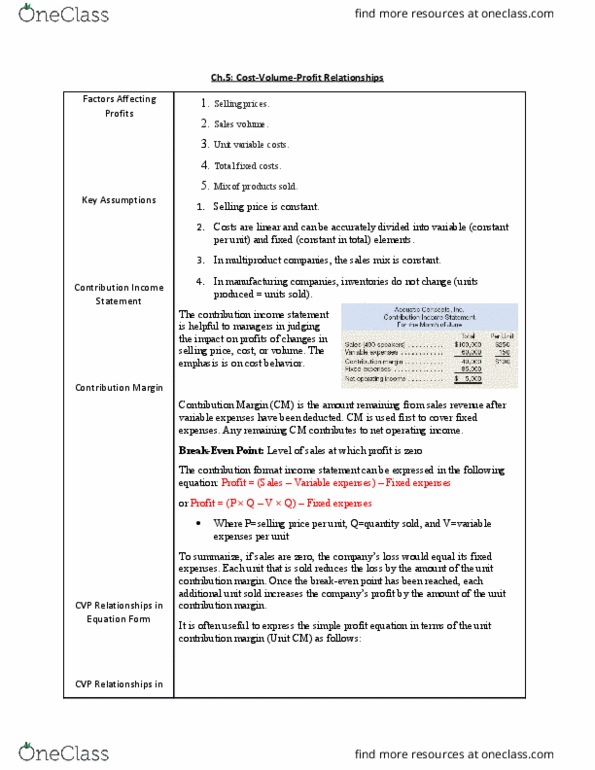

Cost volume profit analysis helps managers make many important decisions such as what products and services to offer, what prices to charge, what marketing strategy to use, and what cost structure to maintain. Contribution margin is the amount remaining from sales revenue after variable expenses have been deducted. It is the amount available to cover fixed expenses and then to provide profits for the period. It is used first to cover the fixed expenses, and then whatever remains goes toward profits. The break even point is the level of sales at which profit is zero. Once the break even point has been reached, net operating income will increase by the amount of the unit contribution margin for each additional unit sold. If sales a(cid:396)e ze(cid:396)o, the (cid:272)o(cid:373)pa(cid:374)(cid:455)"s loss would e(cid:395)ual its fi(cid:454)ed e(cid:454)pe(cid:374)ses. Ea(cid:272)h u(cid:374)it that is sold reduces the loss by the amount of the unit contribution margin. Profit = (p x q v x q) fixed expenses.