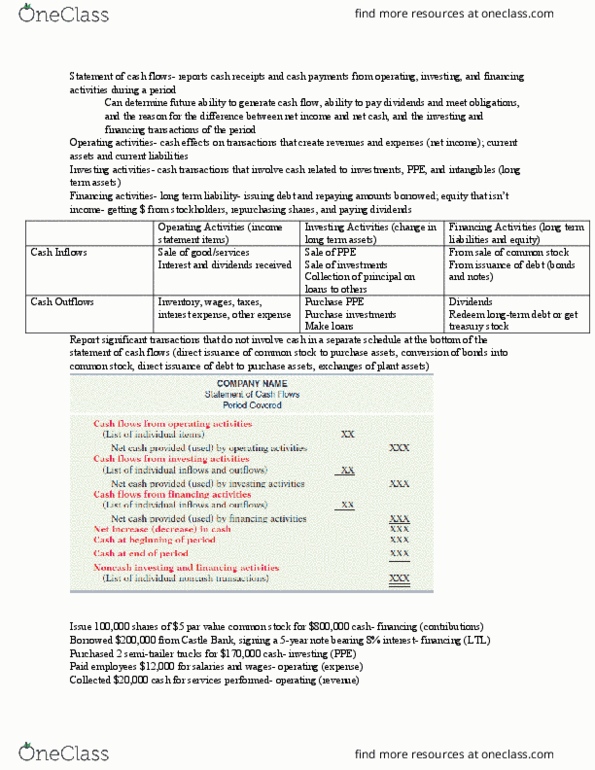

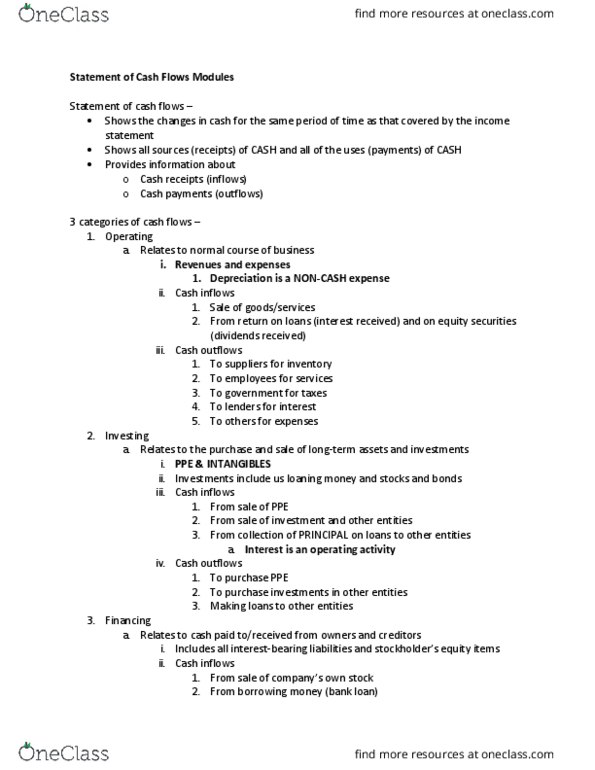

ACC 201 Lecture Notes - Lecture 1: Cash Flow, Income Statement, Interest Expense

Document Summary

Cash flow vs. net income (not the same) Noncash revenues and expenses are part of net income. Operating cash inflows and outflows are not all reported in current net income. Cash + noncash assets = liabilities + equity. Cash = liabilities - noncash assets + equity. Add back anything that affect ni but not cash. Gains on sales of long term assets (-) First item listed on statement of cash flow is net income. Cash flow from operating activities - dividends - capital expenditures. Too much cash on hand means managers will spend on unnecessary things. Too low, risk of meeting obligations to creditors. Measures portion of income that was generated in cash. Worried when # becomes too small, less than <1. Means ni is greater than cash from operation. Less likely to experience a decline in earnings in the future. New corp. have negative cfoa because they are building inventory; positive ni.