COMM 324 Study Guide - Final Guide: Risk-Free Interest Rate, Standard Deviation, Expected Return

16 Apr 2016

School

Department

Course

Professor

Document Summary

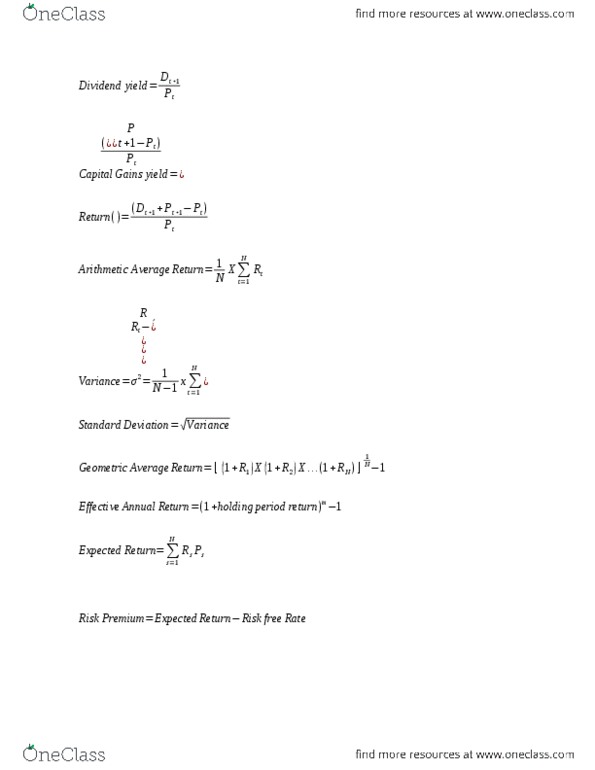

Ytm = the bond discount rate (or yield to maturity) n = the term to maturity (i. e. year t ) F = face (or par) value of the bond. Degree of correlatio n between th e returns of securities anda. Traces the efficient set of portfolios formed from both risky assets and the risk free asset. Relates return to beta (i. e. systematic market risk) not standard deviation (i. e. total risk) The measure of risk used is the standard deviation. All properly priced individual securities and portfolios should lie on the sml, not just the efficient ones ri = rate of return associated with the ith possible state. Pi = probability of the ith state occurring. Formula sheet n = number of days to maturity. Bond equivalent yield: canada t-billsn365pp000,1rbey p = price of the t-bill. Bank discount rate (bd)n360000,1p000,1rbd impossible to compare rbd and rbey directly. Short sale %130100000,15$ p* ,000 = initial margin + sale proceeds =