FIN 701 Study Guide - Credit Risk, Capital Adequacy Ratio

12 Nov 2013

School

Department

Course

Professor

Document Summary

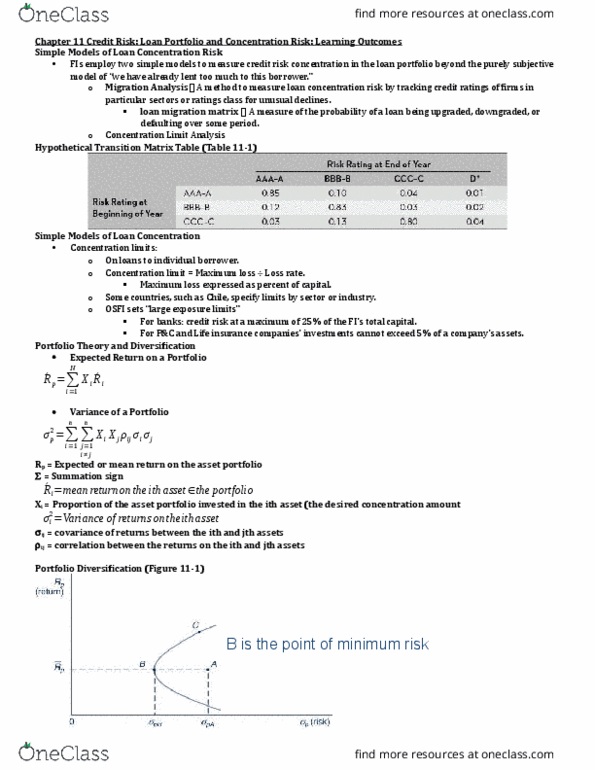

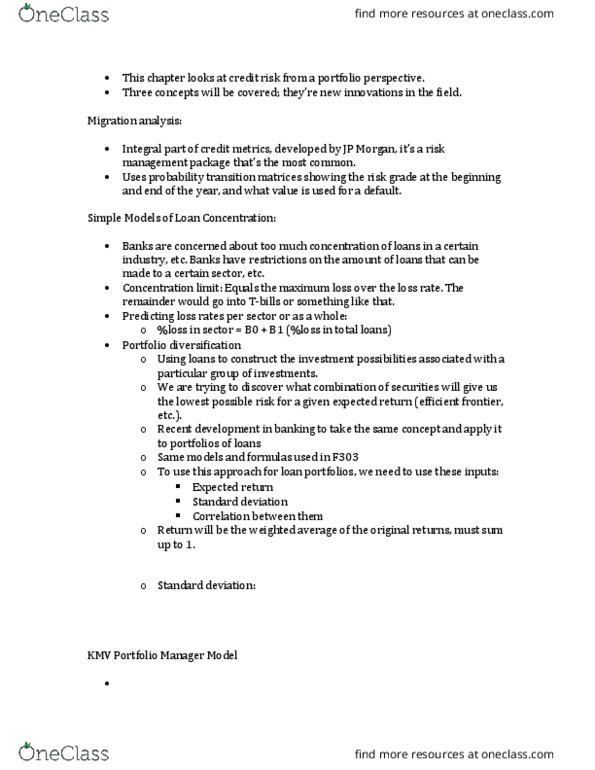

Two simple models to measure credit risk concentration in the loan portfolio: migration analysis method to measure loan concentration risk by tracking credit ratings of firms in particular sectors or ratings class for unusual declines. Proportion of loan portfolio that can go to any single customer by assessing the borrower"s current portfolio, its operating unit"s business plan, its economists" economic projections, and its strategic plans. Portfolio diversification model can be used to measure and control fi"s aggregate credit risk exposure. Modern portfolio theory (mpt) takes advantage of its size, and fi can diversify considerable amounts of credit risk as long as the returns on different assets are imperfectly correlated with respect to their default risk-adjusted returns. Each portfolio mix is efficient in the sense that it offers the lowest risk level to fi manager at each possible level of portfolio returns. Minimum-risk portfolio combination of assets that reduces the variance of portfolio returns to the lowest feasible level.