FIN 701 Study Guide - Monocline, Long Tail, Allianz

18 Sep 2013

School

Department

Course

Professor

Document Summary

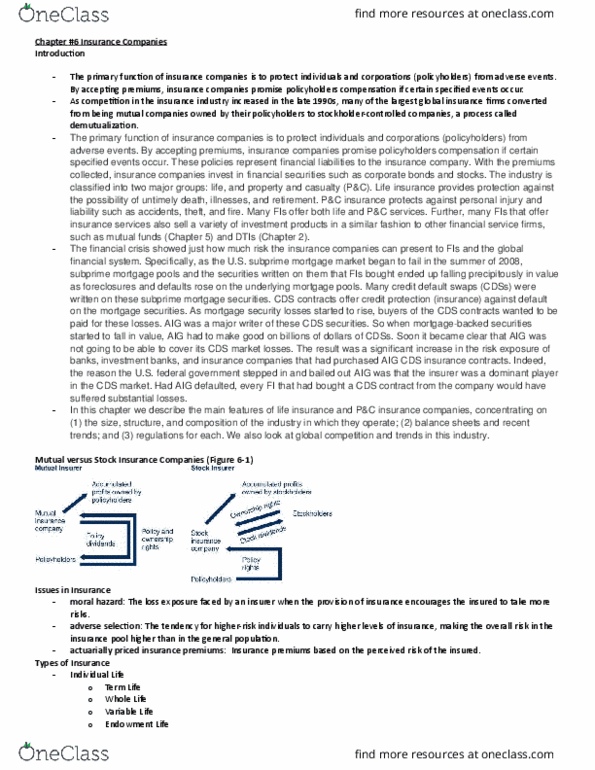

By accepting premiums, insurance companies promise policyholders compensation if certain events occur. Life insurance provides protection against possibility of untimely death, illnesses, and retirement: property insurance protects against personal injury and liability such as accidents, theft, and fire. By pooling risk, life insurance transfers income-related uncertainties from the insured individual to a group. Insurance companies deal with this by establishing different pools of population based on health and related characteristics to determine probability of loss and determining pay out. Actuarially priced insurance premium based on perceived risk of insured. Four basic classes of life insurance: individual life, group, industrial life, and credit life: 63% of total life insurance was for individual life insurance; remaining was group life insurance. Five basic contractual types; first three are traditional forms of life insurance, and last two are newer contracts: term life individual receives a payout contingent on death during coverage period.