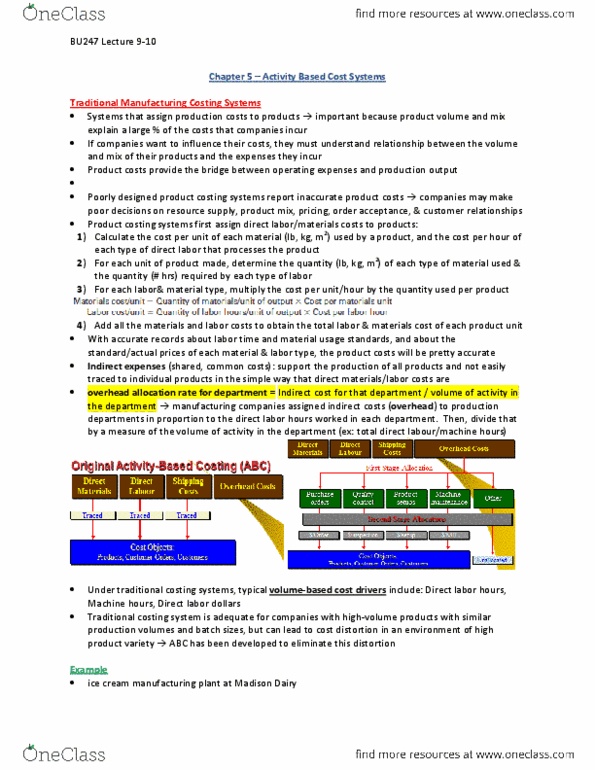

BU247 Final: Managerial Accounting Review (2)

Differences Between ABC and Traditional Product Costs

1. Tradtional costing allocates all manufacturing overhead to products. ABC costing

only assigns manufacturing overhead costs consumed by products to those

products

2. Traditional costing allocates all manufacturing overhead costs using a volume-

related allocation base while ABC costing also uses non-volume related allocation

bases

3. Traditional costing disregards selling and admin expenses since they are

assumed to be period expenses. ABC costing directly traces shipping costs to

products and includes non-manufacturing overhead costs caused by products in the

activity cost pools that are assigned to products

Chapter 6: Cost Behaviour Analysis and Use

Variable and Fixed Cost Behaviour

Cost

In Total

Per Unit

Variable

Total VC is proportional

to the activity level

VC per unit is constant

(ex. telephone

cost/min)

Fixed

Total FC remains

constant

FC per unit goes down

as activity level goes up

Variable Cost – dollar amount varies in direct proportion to changes in the activity

level

Fixed Cost – dollar amount remains constant as the activity level changes

Step-Variable Cost – a resource that is obtainable in large chunks and whose

costs increase/decrease only in response to fairly wide changes in activity

An example of step-variable costs is maintenance

workers. Small changes in the level of production are

not likely to have any effect on the number of

maintenance workers employed. Only fairly wide

changes in the activity level will cause a change in the

number of maintenance workers employed.

find more resources at oneclass.com

find more resources at oneclass.com

Two Types of Fixed Costs:

1) Committed Fixed Costs – long-term, cannot be significantly reduced in short

term (depreciation)

2) Discretionary Fixed Costs – may be altered in the short-term (advertising)

The relevant range of activity for a fixed cost is the range of activity over which

the graph of the cost is flat

Ex. Office space is available at a rental rate of $30,000/year in increments of 1,000

square feet. As the business grows, more space is rented, increasing the total cost

Mixed Costs – a mixed cost has both fixed and variable components

Ways to Analyze Mixed Costs

1) Scattergraph Method

- plot the data points, draw a line through the data points with about an equal

number of points above and below the line

Y = a + bX

If your fixed monthly utility charge

is $40 and your variable cost is

$0.03 per kilowatt hour, and your

monthly activity level is 2,000

kilowatt hours, what is the amount

of your utility bill?

Y = a + bX

Y = $40 + ($0.03 x 2,000) = $100

find more resources at oneclass.com

find more resources at oneclass.com

Now make a quick estimate of variable cost per unit and determine the cost

equation:

2) High-Low Method

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Differences between abc and traditional product costs: tradtional costing allocates all manufacturing overhead to products. Abc costing directly traces shipping costs to products and includes non-manufacturing overhead costs caused by products in the activity cost pools that are assigned to products. Total vc is proportional to the activity level. Vc per unit is constant (ex. telephone cost/min) Fc per unit goes down as activity level goes up. Variable cost dollar amount varies in direct proportion to changes in the activity level. Fixed cost dollar amount remains constant as the activity level changes. Step-variable cost a resource that is obtainable in large chunks and whose costs increase/decrease only in response to fairly wide changes in activity. An example of step-variable costs is maintenance workers. Small changes in the level of production are not likely to have any effect on the number of maintenance workers employed.