ACTG 3110 Study Guide - Midterm Guide: Executory Contract, Cash Flow, Accrual

30 Sep 2013

School

Department

Course

Professor

Document Summary

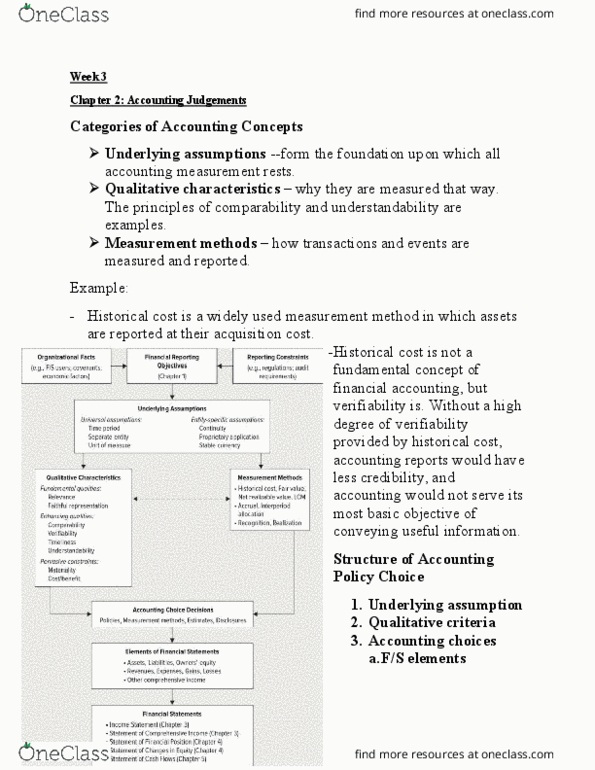

Underlying assumptions basic foundation upon which accounting measurement rests. Qualitative characteristics (qualitative criteria) criteria that"s used to evaluate the options and choose the best methods for a given situation why. Measurement methods different ways financial position and results can be reported (historical cost, revenue recognition) how. Historical cost is used (measurement method) because it is verifiable (qualitative) Make sure the underlying assumptions are valid. Measure the elements of financial statements using situation-specific measurement methods that satisfy the qualitative criteria. Accounting choices for measurement and reporting: underlying assumptions, qualitative criteria, accounting choices, measurement methods, recognition and realization, financial statement elements. Professional judgment process of making choices in accounting being able to rely on judgment in preference to stipulating rigid rules. Can be grouped into 2 general categories: universal assumptions essential in order to make reports feasible and meaningful, entity-specific assumptions very common, but depend on individual entity. Entity-specific assumptions: continuity enterprise will operation for a reasonable future period.