AFA 300 Chapter Notes - Chapter 2: Cash Flow, Income Statement, Executory Contract

20 Sep 2020

School

Department

Course

Professor

Document Summary

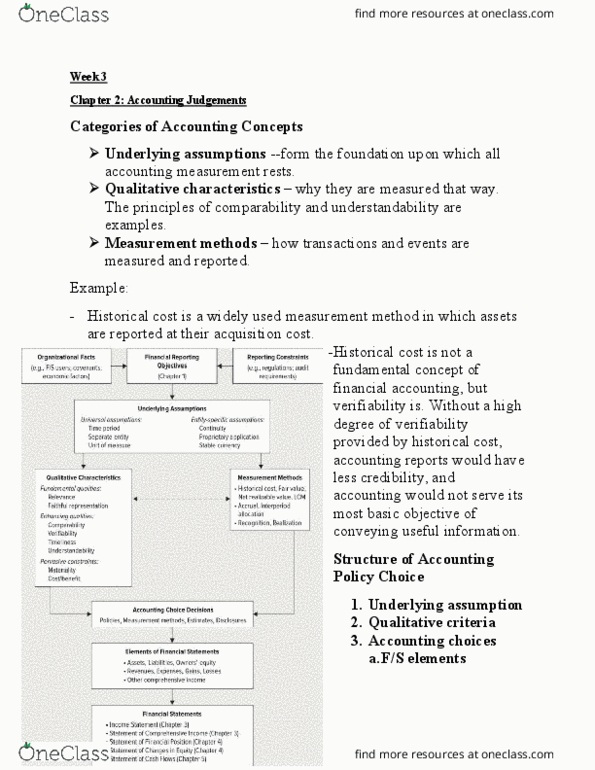

Ethical judgement in accounting: exercise ethical judgments in making choices by acknowledging, users and their specific information needs, motivations of managers, nature of organization"s operations, organizations reporting constraints, such as audit requirements, reporting to securities regulators. If cannot be measured, cannot be reported, and cannot be used for decision making: entity-specific assumptions, proprietary approach: organization"s financial condition and results of operations are reported from the. P. o. v. of owners: payments to owners are capital transactions and not expenses, continuity (going-concern assumption): business entity is expected to continue operations into foreseeable future. Life long enough to recover/use up assets and repay its outstanding liabilities: stable currency: reporting currency is stable over time, not entirely true due to inflation, every dollar of revenue and expense has same value regardless of year. Pervasive constraints: materiality: describe significance of an item. Statement of financial position (balance sheet): assets, owners" equity. Income- revenue, sales, gains: expenses- loses, cost of goods, other comprehensive items (ifrs only)