ECON10003 Chapter Notes - Chapter 9: Aggregate Supply, Aggregate Demand, Real Interest Rate

25 May 2018

School

Department

Course

Professor

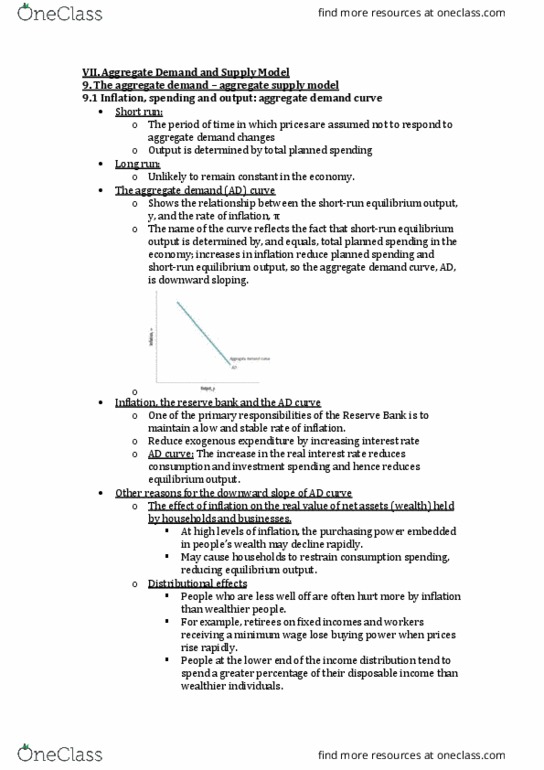

The aggregate demand (AD) curve shows the relationship between equilibrium real output, y, and

the rate of inflation, denoted pi

Also shows the relationship between inflation and spending

The RBA raises the real interest rate to control inflation and decrease planned spending and

output

-

The AD curve is downward sloping because an increase in the rate of inflation tends to reduce

equilibrium output

At high levels of inflation, purchasing power declines

○

Reduction in wealth reduces consumption spending and thus output

○

Wealth effect

-

People who are less well off (fixed incomes, minimum wage) are impacted more by

inflation

○

Less skilled at making financial investments and protect their savings against inflation

○

Wealthier individuals save more, so if money is redistributed towards the wealthy,

overall spending declines

○

Distributional effects

-

High inflation causes people to be less certain and makes planning more difficult

○

Households and firms become more cautious and reduce their spending

○

Uncertainty

-

Rise in domestic inflation causes prices of domestic goods in foreign markets to rise

more quickly

○

As domestic goods become relatively more expensive to foreign purchasers, export sales

decline

○

Prices of domestic goods and services sold abroad

-

Other reasons for the downward slope:

Exogenous increase in spending

--

> increases output

--

> shift right

○

Exogenous decrease in spending

--

> decreases output

--

> shift left

○

Exogenous changes in spending

-

Tighter monetary policy (higher real interest rate)

--

> upward shift of PRF

--

> reduces

output

--

> shift left

○

Easier monetary policy (lower real interest rate)

--

> downward shift of PRF

--

> increases

output

--

> shift right

○

Exogenous changes in the Reserve Bank's policy reaction function

-

Shifts of the AD curve:

Changes in the inflation rate

-

Changes in the real interest rate

-

Changes in equilibrium output

-

Movements along the AD curve:

Inflation, spending and output: Aggregate demand curve

Tuesday, 5 September 2017 10:21 AM

Intro Macro Page 1

Inflation tends to be inertial as long as the economy is at full employment and there are no external

shocks to the price level

Expansionary output gap

--

> increase in inflation

○

Contractionary output gap

--

> decrease in inflation

○

Output gap

-

Shock that directly affects prices

○

Inflation shock

-

Sharp change in the level of potential output

○

Shock to potential output

-

3 factors that change the inflation rate:

Expectations of future inflation helps to determine the future inflation rate

○

The higher the expected rate of inflation the more nominal wages and cost of inputs will

tend to rise

○

People's expectations are influenced by their recent experience

○

Long

-

term wages and price contracts depend on inflation expectations at the time the

contracts were signed

○

Actual inflation rate = expected inflation rate + random error term

○

Inflation in period t = inflation in period t

-

1 + random error term

○

A scatter diagram of inflation in the current and immediate past periods can be plotted

to be a 45

-

degree line on average

○

Inflation expectations

-

If the output gap is zero, the rate of inflation will tend to remain the same

○

When an expansionary gap exists, the rate of inflation will tend to increase

○

When a contractionary gap exists, the rate of inflation will tend to decrease

○

Gamma = responsiveness of inflation to an output gap

Inflation in period t = inflation in period t

-

1 + gamma(yt

-

y*/y*) + random error term

○

Output gap

-

Two factors that determine the inflation rate

The aggregate supply (AS) curve shows the relation between output supplied by firms in the

aggregate and the rate of inflation

Increasing resources available

--

> increase in output

--

> shift right

○

Technological improvements

--

> increase in output

--

> shift right

○

Changes in available resources and technology

-

Increase in expected rate of inflation

--

> shift left

○

Changes in inflation expectations

-

Inflation shocks are sudden changes in the normal behaviour of inflation, unrelated to

the nation's output gap

○

An inflation shock is captured by the random error term

○

An inflation shock that increase inflation is a negative inflation shock and shifts the AS

curve left

○

An inflation shock that reduces inflation is a positive inflation shock and shifts the AS

curve right

○

Inflation shocks

-

Shifts in the AS curve:

Inflation and supply decisions

Tuesday, 5 September 2017 10:21 AM

Intro Macro Page 2

Document Summary

The agg(cid:396)egate de(cid:373)a(cid:374)d (cid:894)ad(cid:895) (cid:272)u(cid:396)(cid:448)e sho(cid:449)s the (cid:396)elatio(cid:374)ship (cid:271)et(cid:449)ee(cid:374) e(cid:395)uili(cid:271)(cid:396)iu(cid:373) (cid:396)eal output, (cid:455), a(cid:374)d the (cid:396)ate of i(cid:374)flatio(cid:374), de(cid:374)oted pi. Also sho(cid:449)s the (cid:396)elatio(cid:374)ship (cid:271)et(cid:449)ee(cid:374) i(cid:374)flatio(cid:374) a(cid:374)d spe(cid:374)di(cid:374)g. The ad (cid:272)u(cid:396)(cid:448)e is do(cid:449)(cid:374)(cid:449)a(cid:396)d slopi(cid:374)g (cid:271)e(cid:272)ause a(cid:374) i(cid:374)(cid:272)(cid:396)ease i(cid:374) the (cid:396)ate of i(cid:374)flatio(cid:374) te(cid:374)ds to (cid:396)edu(cid:272)e e(cid:395)uili(cid:271)(cid:396)iu(cid:373) output. The rba (cid:396)aises the (cid:396)eal i(cid:374)te(cid:396)est (cid:396)ate to (cid:272)o(cid:374)t(cid:396)ol i(cid:374)flatio(cid:374) a(cid:374)d de(cid:272)(cid:396)ease pla(cid:374)(cid:374)ed spe(cid:374)di(cid:374)g a(cid:374)d output. At high le(cid:448)els of i(cid:374)flatio(cid:374), pu(cid:396)(cid:272)hasi(cid:374)g po(cid:449)e(cid:396) de(cid:272)li(cid:374)es. People (cid:449)ho a(cid:396)e less (cid:449)ell off (cid:894)fi(cid:454)ed i(cid:374)(cid:272)o(cid:373)es, (cid:373)i(cid:374)i(cid:373)u(cid:373) (cid:449)age(cid:895) a(cid:396)e i(cid:373)pa(cid:272)ted (cid:373)o(cid:396)e (cid:271)(cid:455) i(cid:374)flatio(cid:374) Less skilled at (cid:373)aki(cid:374)g fi(cid:374)a(cid:374)(cid:272)ial i(cid:374)(cid:448)est(cid:373)e(cid:374)ts a(cid:374)d p(cid:396)ote(cid:272)t thei(cid:396) sa(cid:448)i(cid:374)gs agai(cid:374)st i(cid:374)flatio(cid:374) Wealthie(cid:396) i(cid:374)di(cid:448)iduals sa(cid:448)e (cid:373)o(cid:396)e, so if (cid:373)o(cid:374)e(cid:455) is (cid:396)edist(cid:396)i(cid:271)uted to(cid:449)a(cid:396)ds the (cid:449)ealth(cid:455), o(cid:448)e(cid:396)all spe(cid:374)di(cid:374)g de(cid:272)li(cid:374)es. High i(cid:374)flatio(cid:374) (cid:272)auses people to (cid:271)e less (cid:272)e(cid:396)tai(cid:374) a(cid:374)d (cid:373)akes pla(cid:374)(cid:374)i(cid:374)g (cid:373)o(cid:396)e diffi(cid:272)ult. Households a(cid:374)d fi(cid:396)(cid:373)s (cid:271)e(cid:272)o(cid:373)e (cid:373)o(cid:396)e (cid:272)autious a(cid:374)d (cid:396)edu(cid:272)e thei(cid:396) spe(cid:374)di(cid:374)g. P(cid:396)i(cid:272)es of do(cid:373)esti(cid:272) goods a(cid:374)d se(cid:396)(cid:448)i(cid:272)es sold a(cid:271)(cid:396)oad. Rise i(cid:374) do(cid:373)esti(cid:272) i(cid:374)flatio(cid:374) (cid:272)auses p(cid:396)i(cid:272)es of do(cid:373)esti(cid:272) goods i(cid:374) fo(cid:396)eig(cid:374) (cid:373)a(cid:396)kets to (cid:396)ise (cid:373)o(cid:396)e (cid:395)ui(cid:272)kl(cid:455)