ACTG 3P41 Chapter Notes - Chapter 3: Employment Contract, Employee Benefits, Pension

11 Dec 2016

School

Department

Course

Professor

Document Summary

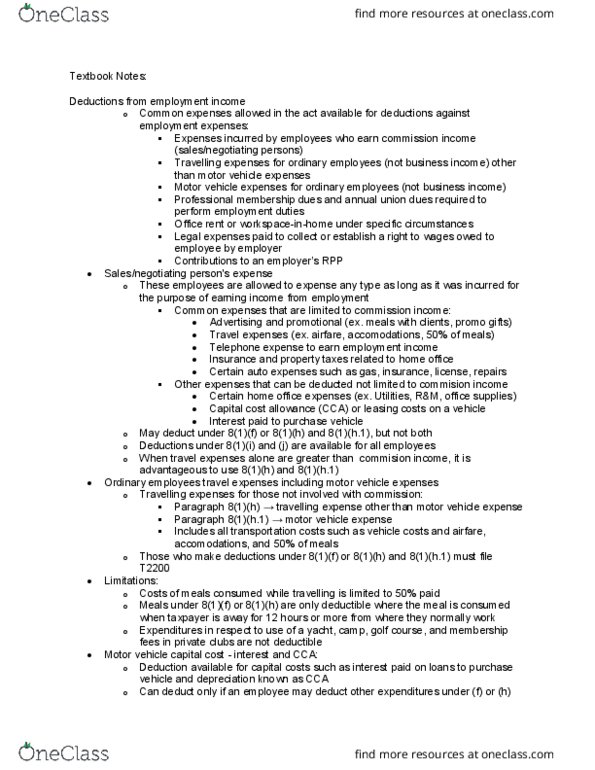

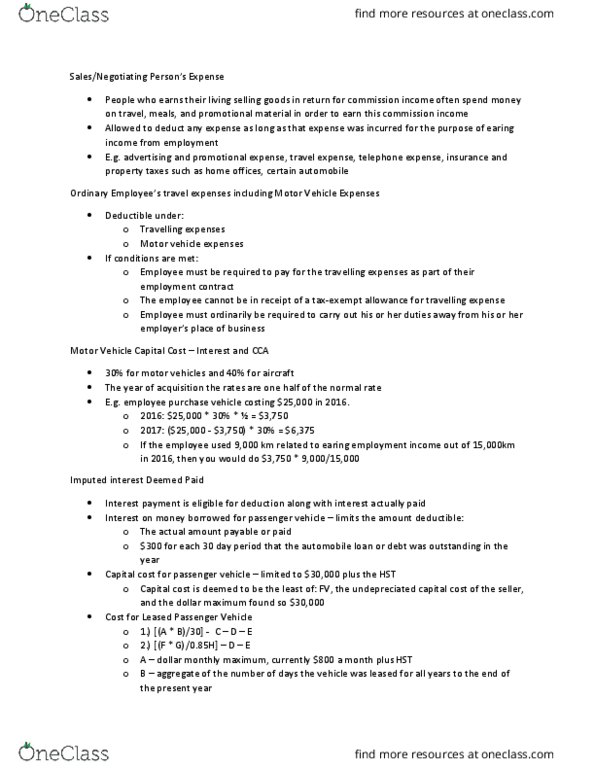

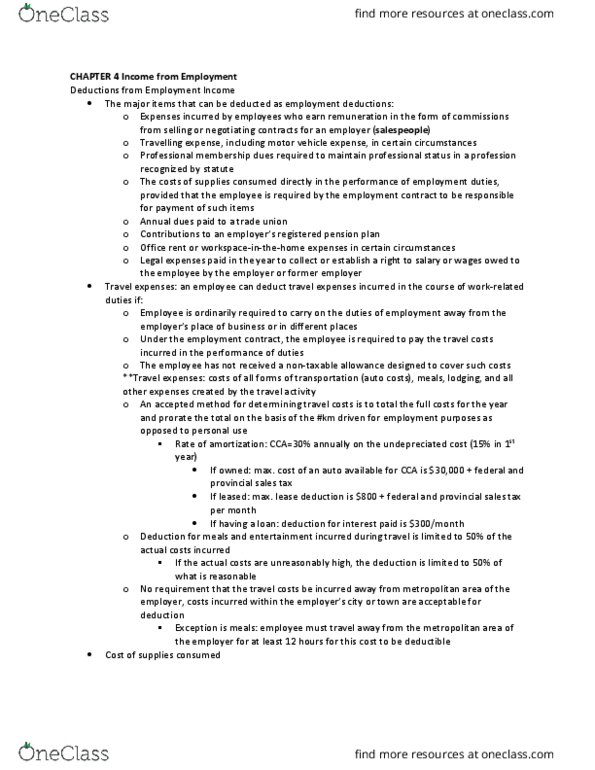

Expense will be denied if incurred to commit offence(pizza guy speed ticket) Allowed to deduct any type of expense as long as that expense was incurred for the purpose of earning income from employment. Limited in terms of dollar value to the amount of commission income. Insurance and property taxes as they relate to a home office insurance, license, repairs, parking). Not limited to commission deductions: home office expenses(utilities, maintenance, repairs, office supplies, long distance phone called, home phone or cell phone, capital cost allowance or leasing costs on a vehicle. Expenditures in use of following not deductible examples: yacht, camp, lodge, golf course, membership or private clubs. These conditions must be met for expenses to be deductible: Employee must be required to pay often expenses as stipulated in the contract of employment. Employee must ordinarily be required to carry on business away from employers place of business. Remuneration must be dependent on volume of sales or contracts.