COMM 305 Chapter Notes - Chapter 7: Sunk Costs, Fixed Cost, The Blenders

7 Apr 2017

School

Department

Course

Professor

Document Summary

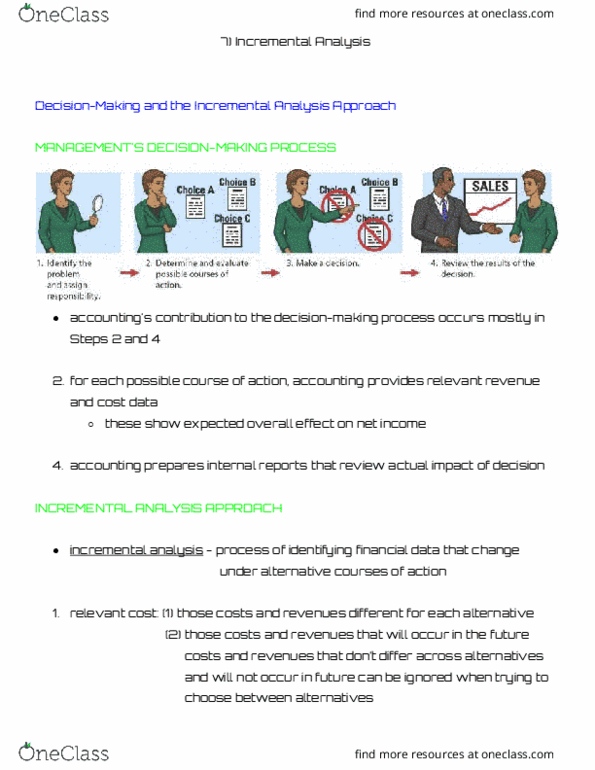

Making decisions is important for management, but the decision process doesn"t always follow the same pattern. Decisions vary in their scope, urgency and importance. We can identify some steps that management often uses in the process: Identify the problem and assign responsibility: determine and evaluate possible courses of action, make a decision, review the results of the decision. Accounting contributes is steps 2 & 4 evaluating the possible sources of action and reviewing the results. For each possible course of action, accounting provides relevant revenue and cost data. Accounting prepares internal reports that review the actual impact of the decision. When making business decisions, management considers financial and non-financial information. Financial information: this is about revenues and costs and their effect on the company"s overall profitability. Non-financial information: this is about factors such as the effect of the decision on employee turnover, the environment, or the company"s overall image in the community.