COMM 305 Chapter 6: comm 305 note

25 Jan 2015

School

Department

Course

Professor

Document Summary

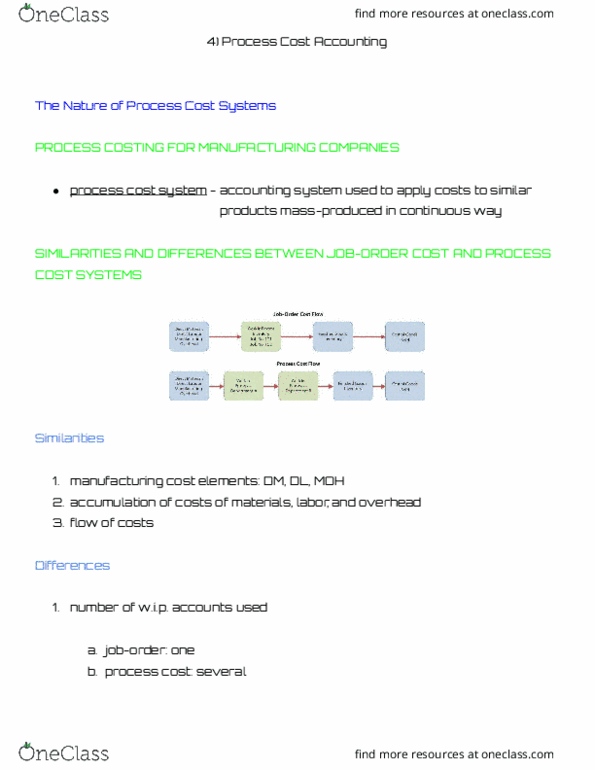

Understand who uses process cost systems and explain the similarities and differences between job-order cost and process cost systems. Explain the flow and assignment of manufacturing costs in a process cost system. Explain the four necessary steps to prepare a production cost report. * debit raw materials costs to raw material inventory. * debit factory labour costs to factory labor. Accumulation of materials and labour costs is the same as in job order costing. * debit raw materials inventory for all purchases of raw materials. * debit factory labour for all factory labour incurred. ***assignment of the 3 manufacturing cost elements to work in process is different. Requires less materials than job order cost system. All labour costs incurred within a production department are a cost of processing. Allocate overhead to departments on an objective and equitable basis. Measure the work done during the period (integer units) Determine cost/ per unit of the completed product.