ECON 208 Chapter Notes -Price Ceiling

27

ECON 208 Full Course Notes

Verified Note

27 documents

Document Summary

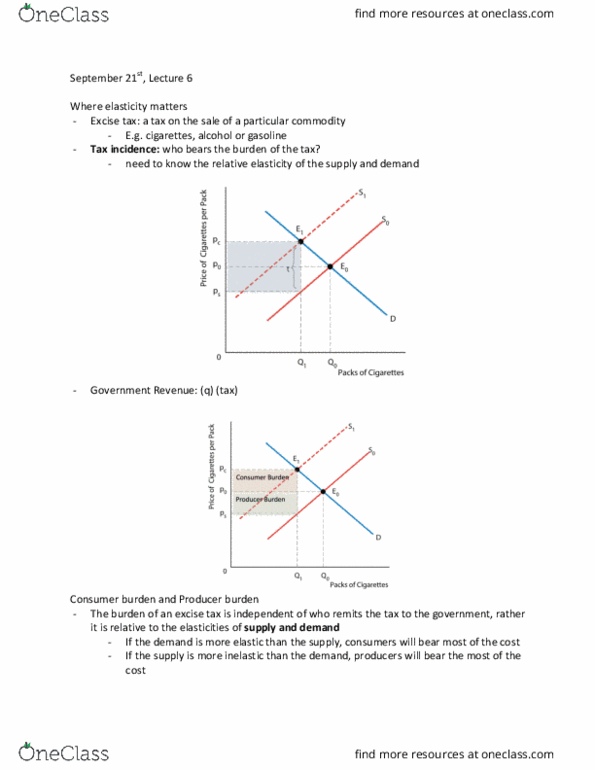

When demand is less elastic than supply, the incidence is significantly higher on the demander. When demand is more elastic than supply, the incidence is significantly lower on the demander: the less elastic is demand relative to supply, the greater the incidence of the tax on consumers (and the less on suppliers) Example: the demand for gasoline is inelastic, therefore the tax incidence is on the consumers. Example: because the inelastic demand of alcohol, the government can increase taxes (which become the burden of the demander rather than the supplier) For demand: change in pd t = 1/b 1/b + 1/d (see webct) The bigger the slope of the demand curve relative to the supply curve, the bigger the tax incidence on consumers. (see the study guide) (see extensions in theory 4-1) Income elasticity of demand ny = %change in quantity demanded %change in income. If ny is greater than zero, the good is said to be normal.