COMMERCE 1AA3 Chapter Notes - Chapter 2: Income Statement, Historical Cost, Revenue Recognition

9 Dec 2016

School

Department

Course

Professor

Document Summary

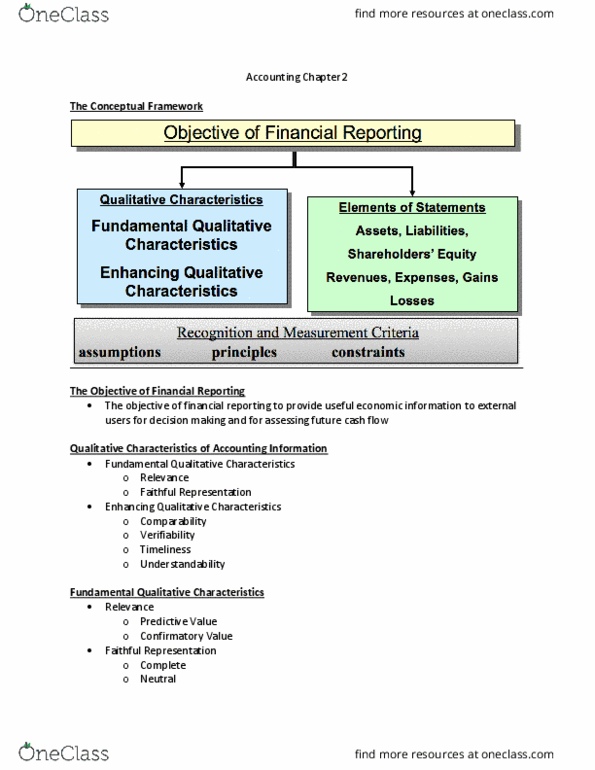

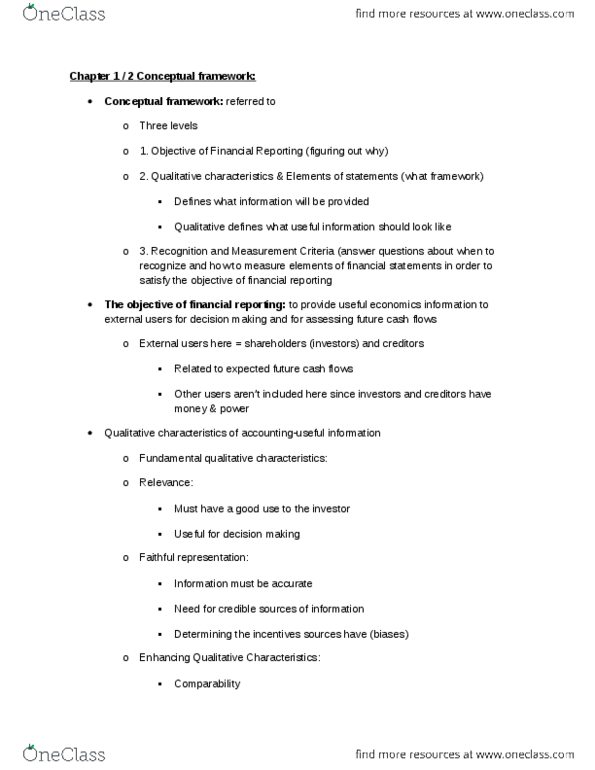

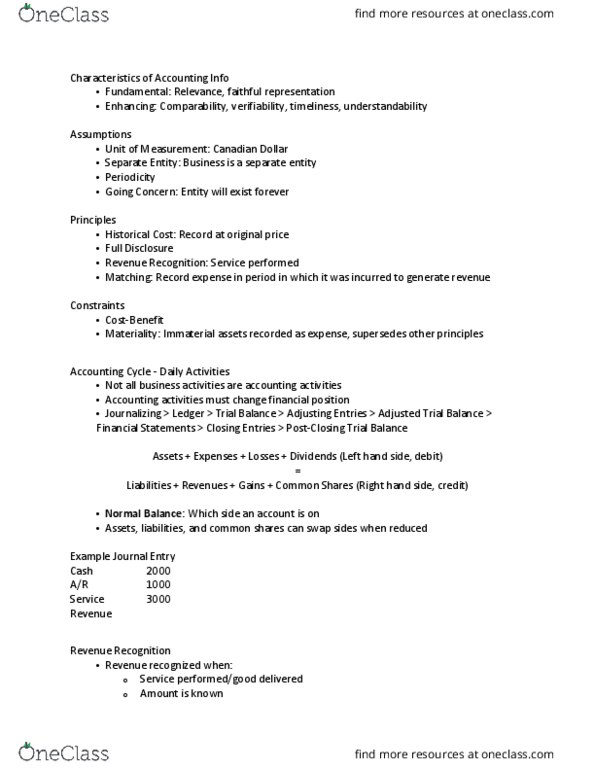

Objective of financial reporting is to provide useful economic information to external users. Assumptions: unit of measurement, separate entity, periodicity, going concern. Principles: historical cost, full disclosure, revenue recognition, matching. Allows you to go against any accounting rule. Historical cost assumption is a result of a going concern assumption. Revenue recognition: service performed, amount known, risk/reward transferred, evidence of an arrangement. Matching principle: must (cid:396)e(cid:272)o(cid:396)d e(cid:454)pense in pe(cid:396)iod (cid:449)hi(cid:272)h it"s in(cid:272)u(cid:396)(cid:396)ed (cid:894)gi(cid:448)en(cid:895) to gene(cid:396)ate (cid:396)e(cid:448)enue, re(cid:272)o(cid:396)d dep(cid:396)e(cid:272)iation pe(cid:396)iodi(cid:272)all(cid:455) to sho(cid:449) it"s (cid:271)een used (cid:894)(cid:396)esult of going concern) Inputs (accounting transactions) processing (methods/guidelines) outputs (financial statements) Must change financial position of company to be accounting activity. Accounting cycle: journalizing, posting entries to ledger, trial balance, end of period adjusting entries, adjusted trail balance, financial statements, closing entries, post-closing trail balance. Assets, liabilities, common shares can swap debit or credit. Anything you do must affect two accounts. Ledger a book that has separate pages for each accounting (each has debit/credit sides)