COMMERCE 1AA3 Chapter Notes - Chapter 12: Cash Flow Statement, Current Liability, Cash Flow

11 Dec 2016

School

Department

Course

Professor

Document Summary

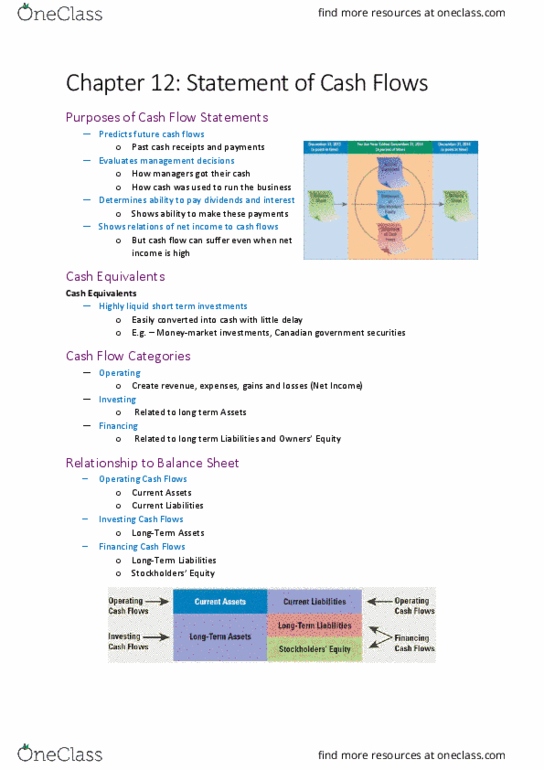

Provide information about cash receipts, cash payments, and the net changes in cash resulting from operating, investing, and financing activities. Operating: income statement items, current assets, and current liabilities: relate to transactions that make up net income (create revenue, expenses, gains and losses, most important activity for a business. Investing: long term assets and investments (purchase and sale of long term assets: cash inflows/outflows related to resources used for generating future income. Fi(cid:374)a(cid:374)(cid:272)i(cid:374)g: lo(cid:374)g te(cid:396)(cid:373) lia(cid:271)ilities a(cid:374)d ow(cid:374)e(cid:396)"s e(cid:395)uity ((cid:272)ha(cid:374)ges i(cid:374) size a(cid:374)d (cid:272)o(cid:373)positio(cid:374) of e(cid:395)uity and borrowing) Issuance and acquisition of company, shares, payments of dividends, cash proceeds from loans, bonds and notes, and repayment of amounts borrowed (long and short term borrowings) Add items that decrease income but do not affect cash: depreciation/amortization expense, losses on disposal of assets (both current and long term, decreases in current assets. Subtract items that increase net income but do not affect cash: gains on disposal of assets (current and long term)