COMMERCE 4AD3 Chapter Notes - Chapter 8: Audit Evidence, Asset, Purchase Order

29 Nov 2017

School

Department

Course

Professor

Document Summary

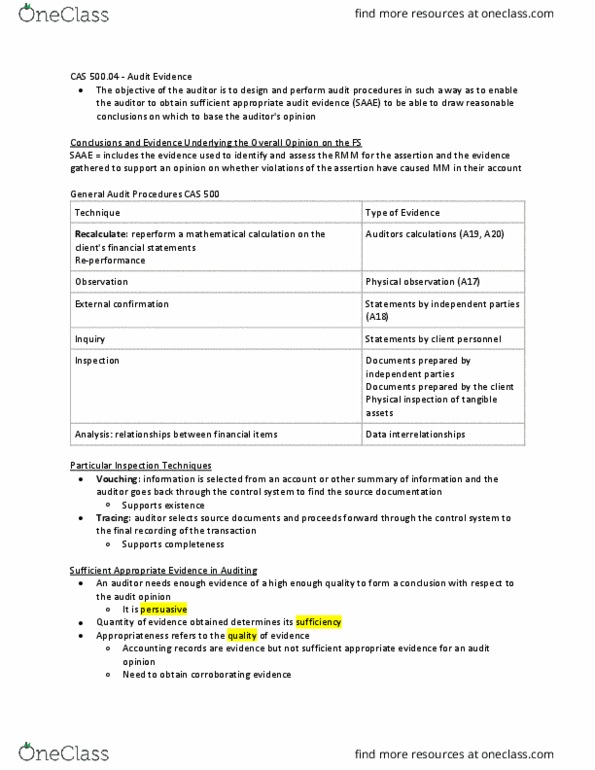

Session 6 - audit evidence & assurances (ch. Documents prepared by independent parties ordinary and formal authoritative documents (bank statements, invoices from suppliers, news) Documents prepared by the auditee (f/s, memos, payroll, invoices for payables and sales, inventory count) Looking at records, documents or assets having physical substance. Reliable evidence for existence and supports valuation but not ownership. Vouching: auditor selects sample of f/s item from account and works backwards through control system to find & examine source documents. E. g. for sales invoice, examining journal entry, sales summary, sales invoice, shipping documents & customer purchase order. Tracing: auditor selects sample of source documents and work forward through control system to final recording of transaction. E. g. sample of payroll payments traces to cost & expense account or. Cash receipt traced to a/r. supports completeness and supplements evidence from vouching. Reduces sampling risk by scanning items not in sample. Gives evidence of existence & completeness, cut-off of material transactions.