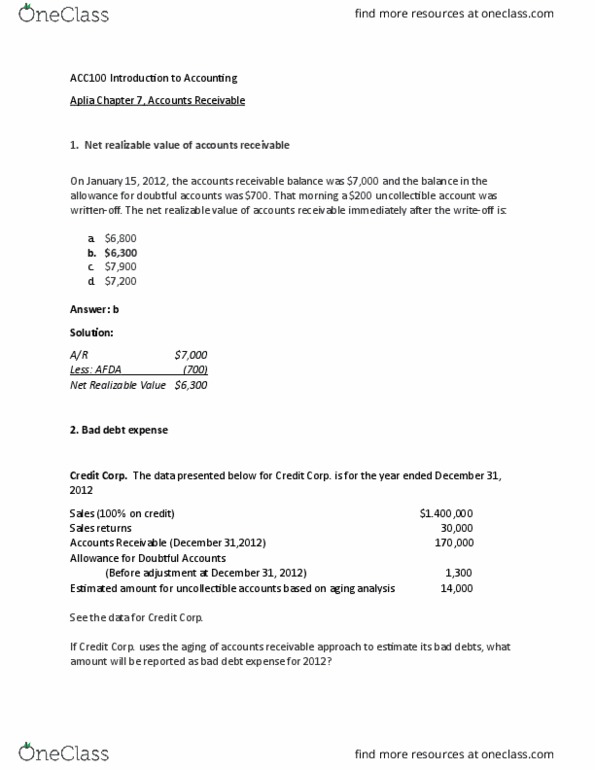

ACC 100 Chapter Notes - Chapter 7: Subledger, Accounts Receivable, General Ledger

21 Nov 2013

School

Department

Course

Professor

Document Summary

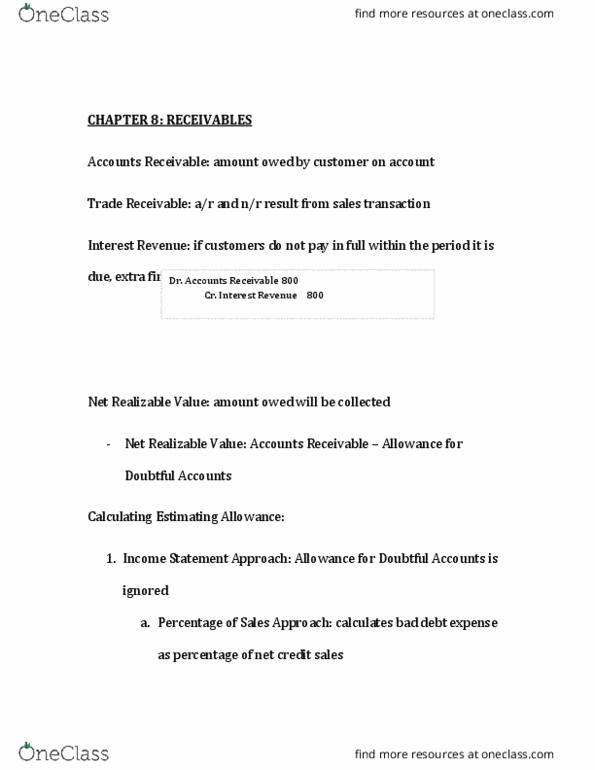

Subsidiary ledger: tracks the balance owed by each customer; the detail for a number of individual items that collectively make up a single general ledger account. Control account: the general ledger account that is supported by a subsidiary ledger. Subsidiary ledger does not take the place of the control account in the general ledger. Direct write-off method: the recognition of bad debts expense at the point an account is written off as uncollectible. Under direct write-off method, an expense increases, and under the allowance method an allowance account is reduced. When an individual wants to restore his credit and pays back, there are 2 adjusting entries: previously written-off account is reversed, the collection of cash from the individual is recorded. Bad debts expense decrease (expense) ( to calculate, get the percentage of the credit under a/c less the balance in doubtful. Allowance for doubtful accounts decreases (asset: aging of accounts receivable.