ACC 100 Chapter Notes - Chapter 7: Promissory Note, Subledger, General Ledger

28 Jun 2018

School

Department

Course

Professor

ACC - Chapter 7

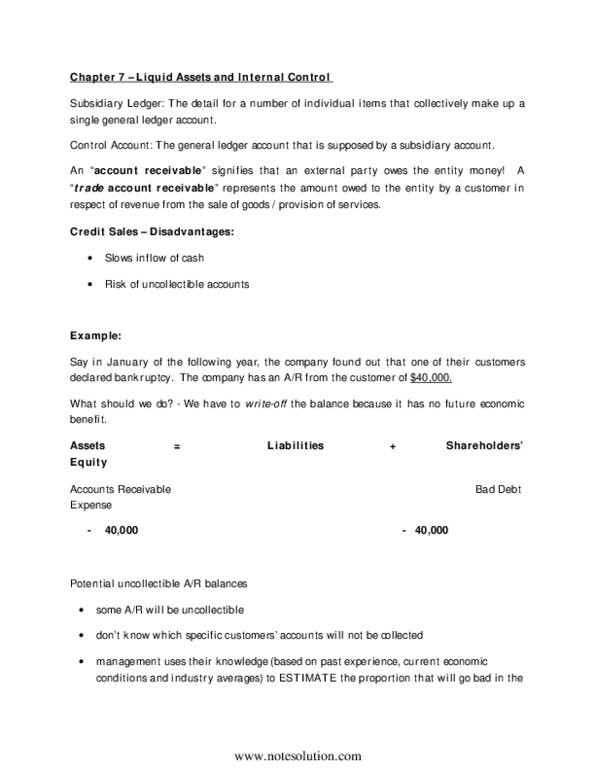

Subsidiary ledger - the detail for a number of individual items that collectively

make up a single general ledger account

Control account - the general ledger account that is supported by a subsidiary

ledger

A subsidiary ledger does not take the place of the control account in the general

ledger

The balances of the accounts that make up the subsidiary ledger should total to the

single balance in the related control account

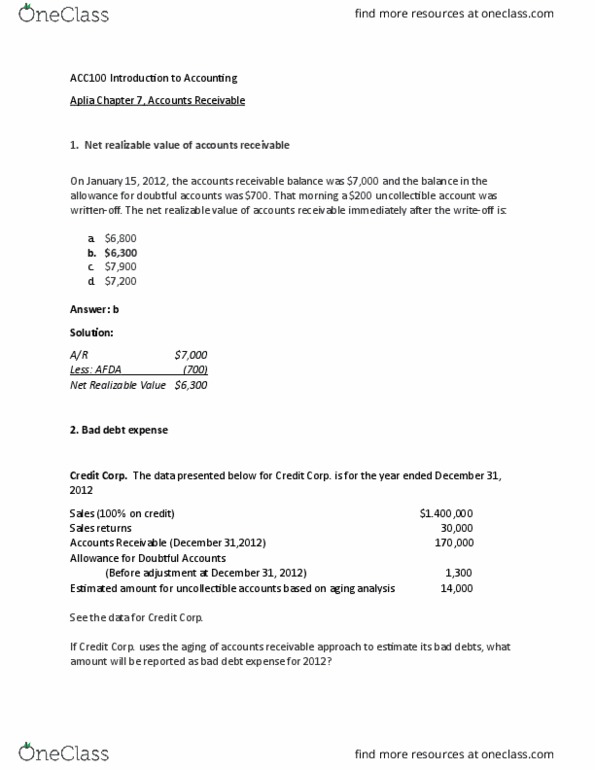

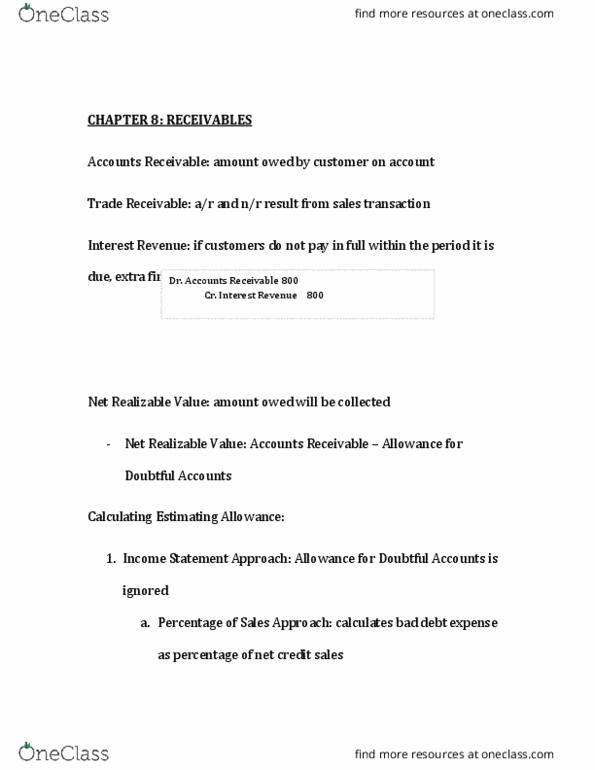

Method accounts for bad debts

Direct write-off method - the recognition of bad debts expense at the point an

account is written off as uncollectible (using bad debts expense and A/R)

An expense is increased

Allowance method - method of estimating bad debts on the basis of either the net

credit sales of the period or the A/R at the end of the period (using bad debts

expense and allowance for doubtful accounts) *contra asset

The allowance account is reduced

Whether the direct write-off or allowance method, the entry to write off a specific

customers account reduces A/R

Approaches to the allowance method for bad debts:

Percentage of net credit sales approach - company being able to use the past

relationships between bad debts and net credit sales to predict bad debt amounts

Under percentage of net credit sales approach, the balance in the allowance

account is ignored, and the bad debts expense is simply a percentage of the

sales of the period

Percentage of A/R approach - estimate bad debts by relation them to the balance in

the A/R account at the end of the period rather than to the sales of the period

Under percent of account receivable approach the balance in the allowance

account must be considered

Also called the balance sheet method - this method estimates the balance of

allowance for doubtful accounts (a balance sheet number) using A/R

(another balance sheet number)

Aging schedule - form used to categorize the various individual accounts receivable

according to the length of time each has been outstanding

Credit card draft - a multiple-copy document used by a company that accepts a

credit card for a sale

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Subsidiary ledger - the detail for a number of individual items that collectively make up a single general ledger account. Control account - the general ledger account that is supported by a subsidiary ledger. A subsidiary ledger does not take the place of the control account in the general ledger. The balances of the accounts that make up the subsidiary ledger should total to the single balance in the related control account. Direct write-off method - the recognition of bad debts expense at the point an account is written off as uncollectible (using bad debts expense and a/r) Whether the direct write-off or allowance method, the entry to write off a specific customers account reduces a/r. Approaches to the allowance method for bad debts: Percentage of net credit sales approach - company being able to use the past relationships between bad debts and net credit sales to predict bad debt amounts.