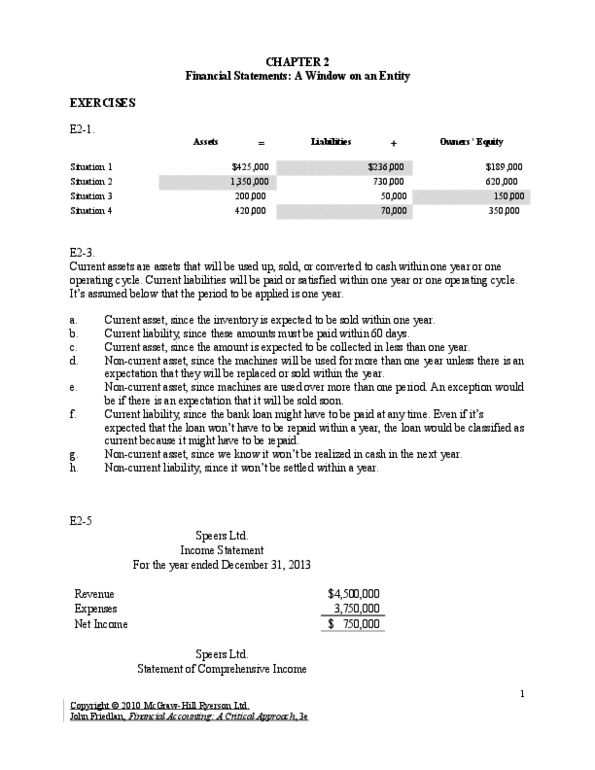

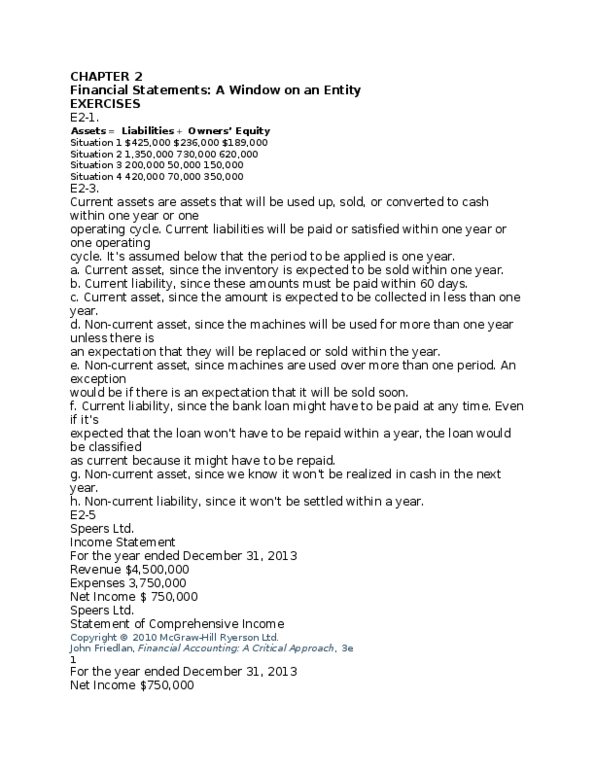

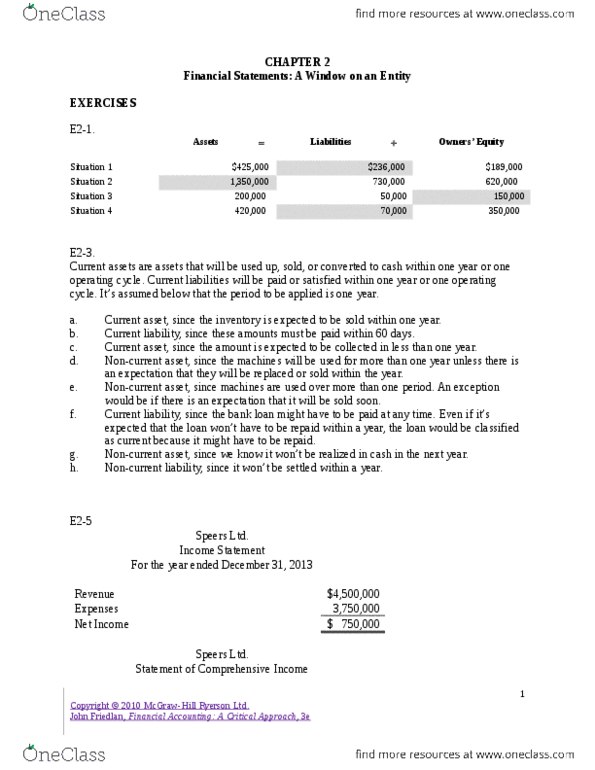

ACC 110 Chapter Notes - Chapter 2: Cash Flow Statement, Retained Earnings, Current Liability

Document Summary

Get access

Related Documents

Related Questions

| Financial Information for Case9-1 | |||

| Industy Wide | |||

| Balance Sheets | |||

| Years Ended December 31, 2014and 2015 | |||

| 2015 | 2014 | ||

| Assets | |||

| Current Assets: | |||

| Cash | $ 30,000 | $ 25,000 | |

| Accounts receivable | 110,000 | 90,000 | |

| Inventories | 100,000 | 80,000 | |

| Total Current Assets | 240,000 | 195,000 | |

| Fixed Assets; | |||

| Plant and equipment | 250,000 | 220,000 | |

| Less accumulated depreciation | (100,000) | (65,000) | |

| Land | 50,000 | 50,000 | |

| Total Fixed Assets | 200,000 | 205,000 | |

| Total Assets | $ 440,000 | $ 400,000 | |

| Liabilities and Equity | |||

| Current Liabilities: | |||

| Accounts payable | $ 58,000 | $ 50,000 | |

| Notes payable-due within one year | 50,000 | 50,000 | |

| Accrued liabilities | - | - | |

| Total Current Liabilities | 108,000 | 100,000 | |

| Long Term Liabilities | 32,000 | 20,000 | |

| Total Liabilities | 140,000 | 120,000 | |

| Stockholders' Equity: | |||

| Common stock | 100,000 | 100,000 | |

| Retained earnings | 200,000 | 180,000 | |

| Total Stockholders' Equity | 300,000 | 280,000 | |

| Total Liabilities and Equty | $ 440,000 | $ 400,000 | |

| Industry Wide | |||

| Income Statement | |||

| Years Ended December 31, 2014and 2015 | |||

| Revenues | $ 1,100,000 | $ 1,000,000 | |

| Cost of goods sold | (700,000) | (650,000) | |

| Gross margin | 400,000 | 350,000 | |

| Operating expenses | (275,000) | (255,000) | |

| Operating income | 125,000 | 95,000 | |

| Interest expense | (15,000) | (15,000) | |

| Income before taxes | 110,000 | 80,000 | |

| Income taxes | (44,000) | (32,000) | |

| Net income | $ 66,000 | $ 48,000 | |

| Financial Information for Case9-1 | |||

| Industy Wide | |||

| Balance Sheets | |||

| Years Ended December 31, 2014and 2015 | |||

| 2015 | 2014 | ||

| Assets | |||

| Current Assets: | |||

| Cash | $ 30,000 | $ 25,000 | |

| Accounts receivable | 110,000 | 90,000 | |

| Inventories | 100,000 | 80,000 | |

| Total Current Assets | 240,000 | 195,000 | |

| Fixed Assets; | |||

| Plant and equipment | 250,000 | 220,000 | |

| Less accumulated depreciation | (100,000) | (65,000) | |

| Land | 50,000 | 50,000 | |

| Total Fixed Assets | 200,000 | 205,000 | |

| Total Assets | $ 440,000 | $ 400,000 | |

| Liabilities and Equity | |||

| Current Liabilities: | |||

| Accounts payable | $ 58,000 | $ 50,000 | |

| Notes payable-due within one year | 50,000 | 50,000 | |

| Accrued liabilities | - | - | |

| Total Current Liabilities | 108,000 | 100,000 | |

| Long Term Liabilities | 32,000 | 20,000 | |

| Total Liabilities | 140,000 | 120,000 | |

| Stockholders' Equity: | |||

| Common stock | 100,000 | 100,000 | |

| Retained earnings | 200,000 | 180,000 | |

| Total Stockholders' Equity | 300,000 | 280,000 | |

| Total Liabilities and Equty | $ 440,000 | $ 400,000 | |

| Industry Wide | |||

| Income Statement | |||

| Years Ended December 31, 2014and 2015 | |||

| Revenues | $ 1,100,000 | $ 1,000,000 | |

| Cost of goods sold | (700,000) | (650,000) | |

| Gross margin | 400,000 | 350,000 | |

| Operating expenses | (275,000) | (255,000) | |

| Operating income | 125,000 | 95,000 | |

| Interest expense | (15,000) | (15,000) | |

| Income before taxes | 110,000 | 80,000 | |

| Income taxes | (44,000) | (32,000) | |

| Net income | $ 66,000 | $ 48,000 | |

1. Calculate the current ratio and average collection period foraccounts receivable, inventory turnover, gross margin percentage,and return on equity for 2014 and 2015 for the JordanCorporation.

2. Calculate the current ratio and average collection period foraccounts receivable, inventory turnover, gross margin percentage,and return on equity for the Industry.

3. Compare the performance of the Jordan Corporation between2014 and 2015 and comment on the trend of each ratio.

4. Compare the performance of the Jordan Corporation in 2015 tothe industry averages and comment on each.

Required - Using the attached- below- financial statements for Coca-Cola calculate the following ratios for 2014 - Hint: use excel to set up the formulas and amounts to calculate (see below chart)

https://www.sec.gov/Archives/edgar/data/21344/000002134415000005/a2014123110-k.htm

| Liquidity ratio | |

| Current assets | 92023 |

| Current liabilities | 32374 |

| Current ratio is current asset/current liabilities | 92023/32374= 2.84 |

| Quick assets=current assets- inventory + prepaid expenses | 92023-3100+3066= 91989 |

| Quick ratio is quick assets/current liabilities | 91989/32374= 2.84 |

| Calculate debt to equity ratio= Total liabilities/ total stockholder equity | |

| Times interest earned= Earnings before interest and taxes (EBIT)/interest expense | |

| Return on Net Operating Assets â RNOA Net Operating assets RNOA= NPOAT/Average NOA | |

| Net Operating Profit After Taxes â NOPAT Net operating profit after taxes= net income- (nonperatinge revenues-nonoperating expenses)x(1-marginal tax rates) | |

| Net Operating Profit Margin â NOPM NPOM= NOPAT/Sales Revenue | |

| Net Operating Asset Turnover â NOAT NOAT= Sales/Average NOA |

| Note 1 | Coca-Cola | ||||

| Operating Assets | |||||

| Total assets - Non-operating assets | |||||

| (ie NOA = Total assets less Short-term investments + Other investments | |||||

| Operating Liabilities | |||||

| Total liabilities - Non-operating liabilities | |||||

| ie NOL = Total liabilities - Loans and notes payable + Current maturities of long-term debt+Long-term debt) | |||||