ACC 406 Chapter Notes - Chapter 11: Stabilisation Force In Bosnia And Herzegovina, Variable Cost

28 Jun 2018

School

Department

Course

Professor

ACC – Chapter 11 – Flexible Budgets and Overhead Analysis

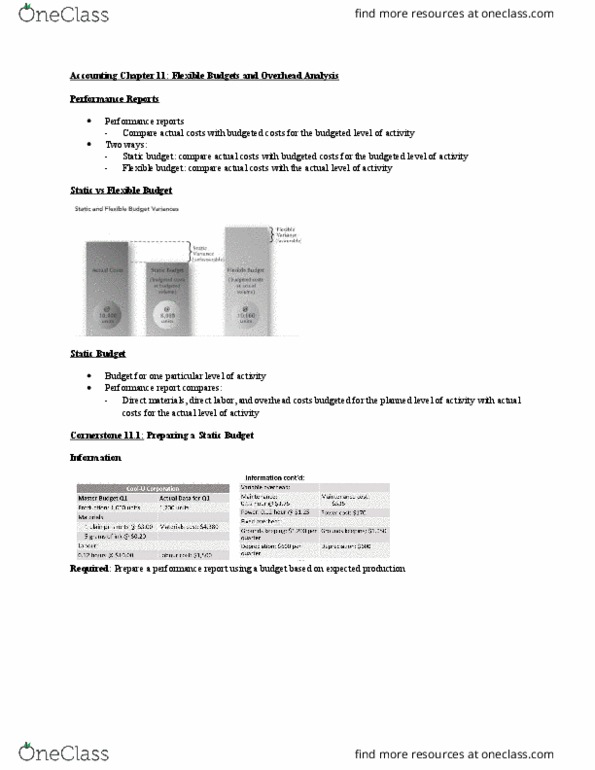

A performance report compares actual costs with budgeted costs

A static budget is a budget for a particular level of activity usually prepared at the

beginning of the period

oCompare the actual costs with the budgeted costs from the master budget to

prepare performance report

A flexible budget enables a firm to compute expected costs for a range of activity levels.

The key to flexible budgeting is knowledge of fixed an variable cost

oBefore the fact – helps managers deal with uncertainty by allowing them to see

the expected outcomes for a range of activity levels. It can be used to generate

financial results for a number of plausible scenarios

oAfter the fact – the budget for the actual level of activity achieved in the period.

Used to compute what costs should have been for the actual level of activity

Flexbile budgets are some times referred to as variable budgets

A difference between the actual amount and the flexible budget amount is the flexible budget

variance

To measure whether or not a manager accomplishes their goals, the static budget is used

Four variance method – 1. Overhead is divided into fixed and variable categories 2. Two

variances are calculated for each category 3. Total variable overhead variance is divided into

the variable overhead spending variance and the variable overhead efficiency variance 4. The

total fixed overhead variance is divided into the fixed overhead spending variance and the fixed

overhead volume variance

Total variable overhead variance is the difference between total actual variable overhead and

applied variable overhead

AH – actual direct labour hours

SH – standard direct labour hours that should have been worked for actual units produced

AVOR – actual variable overhead rate

SVOR – standard overhead rate

The variable overhead spending variance measures the aggregate effect of differences

between the actual variable overhead rate (AVOR) and the standard variable overhead rate

(SVOR)

AVOR = actual overhead rate / actual hours

Variable overhead spending variance = (AVOR x AH) – (SVOR x AH)

= (AVOR – SVOR)xAH

The variable overhead efficiency variance measures the change in the actual variable overhead

that occurs because of efficient or inefficient use of direct labour

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Acc chapter 11 flexible budgets and overhead analysis. A performance report compares actual costs with budgeted costs. A static budget is a budget for a particular level of activity usually prepared at the beginning of the period: compare the actual costs with the budgeted costs from the master budget to prepare performance report. A flexible budget enables a firm to compute expected costs for a range of activity levels. The key to flexible budgeting is knowledge of fixed an variable cost: before the fact helps managers deal with uncertainty by allowing them to see the expected outcomes for a range of activity levels. It can be used to generate financial results for a number of plausible scenarios: after the fact the budget for the actual level of activity achieved in the period. Used to compute what costs should have been for the actual level of activity. Flexbile budgets are some times referred to as variable budgets.