ACC 410 Chapter Notes - Chapter 1: Organizational Ethics, Specific Performance, Management Accounting

13 Jun 2011

School

Department

Course

Professor

Document Summary

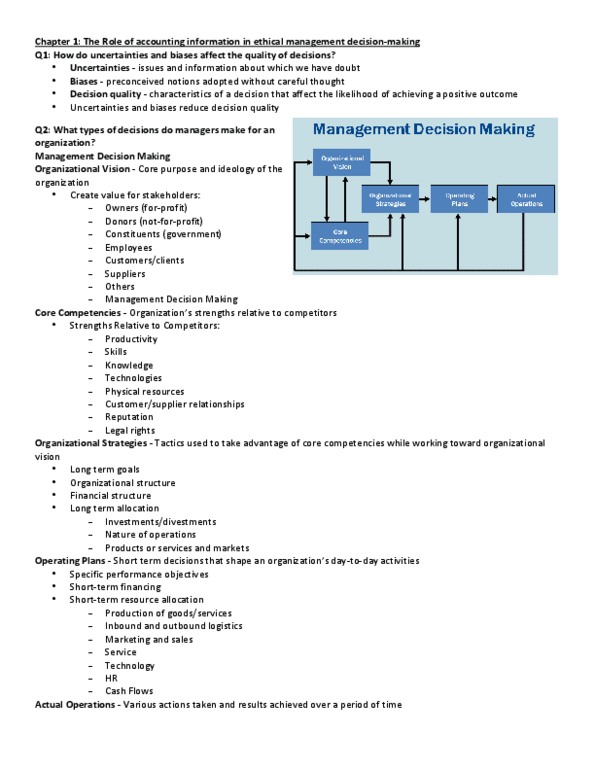

Uncertainties are issues and information about which we have doubt. For example: the exact level of future sales for a product is uncertain. (unable to assume the company"s future and performance) Therefore it is difficult to attain an exact response to the performance of a business, which hinders one from substantially making the correct decisions. Personal example: this course seems to be extremely difficult, the chances of me achieving an overall grade of 75% in the course is uncertain. Biases are preconceived notions adopted without careful thought. For example: a manager who dislikes change might automatically reject a proposal that would alter operations and improve efficiency. (making decisions based on preference, or past experience which have ultimately influence your perception on certain situations) Thus, biases often lead individuals to make poor decisions, since they base their decisions on personal preference or past experience, disregarding the ethical decision.