ACC 100 Chapter Notes - Chapter 1-6: Statement Of Changes In Equity, Retained Earnings, Current Asset

21 Apr 2011

School

Department

Course

Professor

Document Summary

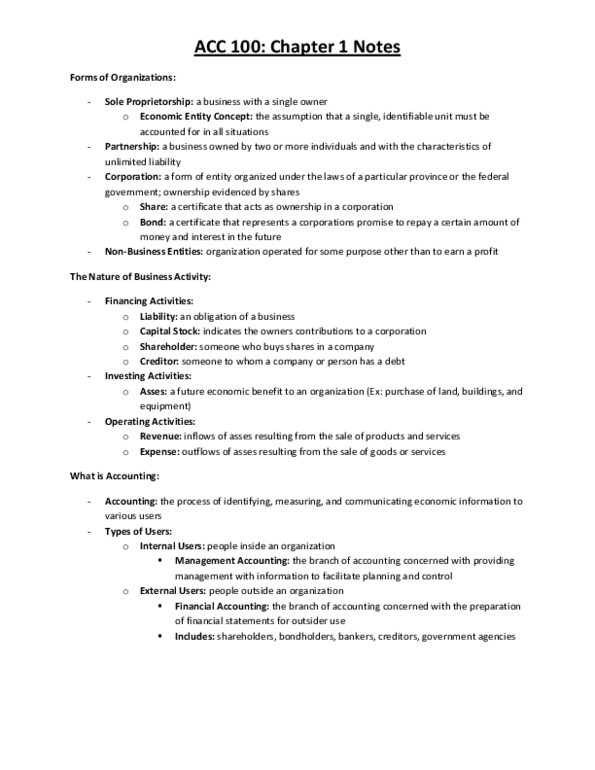

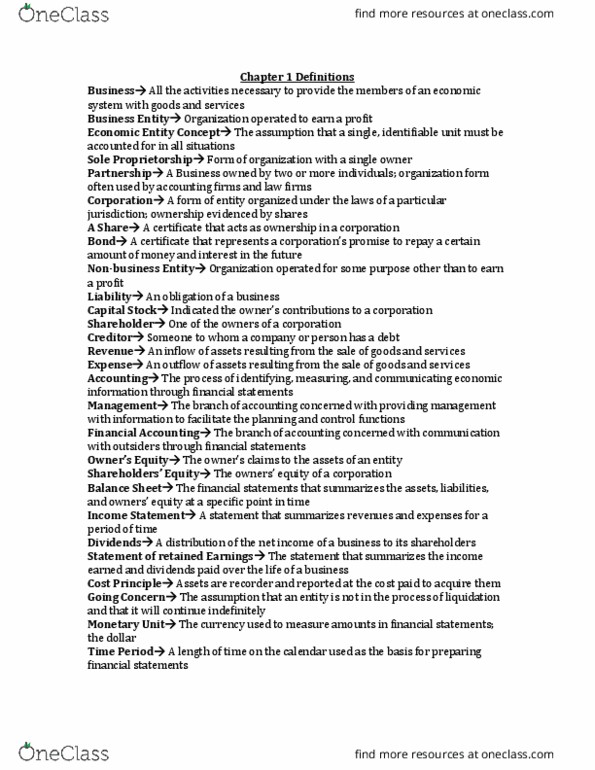

All activities necessary to provide the members of an economic system with goods and service. The assumption that a single, identifiable unit must be accounted for in all situations. Sole proprietorship: form of a organization with a single owner. A business owned by two or more individuals; organization form often used by accounting firms and law firms. A form of entity organized under the laws of a particular jurisdiction; ownership evidenced by shares. A certificate that acts as ownership in a corporation. A certificate that represents a corporation s promise to repay a certain amount of money and interest in the future. Organization operated for some purpose other than to earn a profit an obligation of a business. Indicates the owners contributions to a corporation one of the owners of a corporation. An inflow of assets resulting to the sales of goods and services. An outflow of assets resulting to the sales of goods and services.