ACC 110 Chapter Notes - Chapter 3: General Ledger, Trial Balance, Accrual

1 Dec 2011

School

Department

Course

Professor

Document Summary

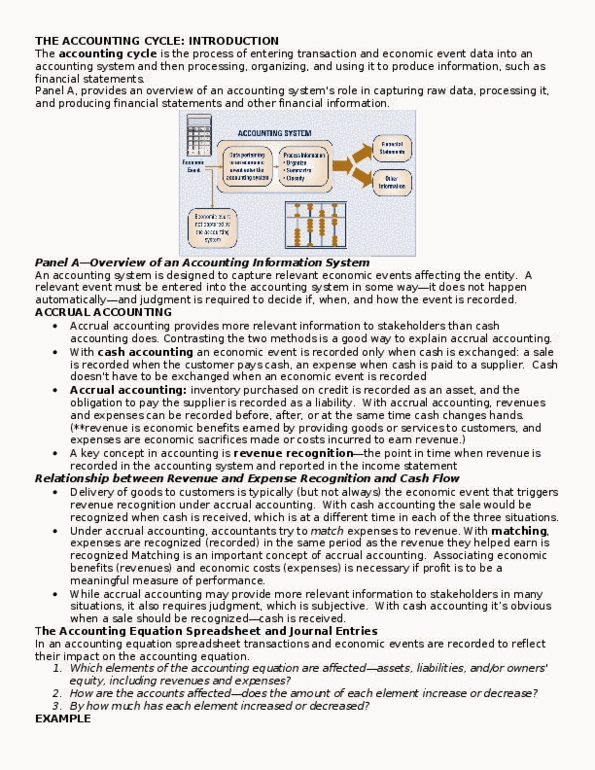

The accounting cycle - the process of entering transaction and economic event data into an accounting system and the processing, organizing, and using it to produce information, such as financial statements. Start of the fiscal period -> transaction or economic event -> prepares journal entry in the general journal -> post journal entry to the general ledger. End of the fiscal period -> prepare and post adjusting journal entries -> prepare the trial balance -> prepare the financial statements -> record and pot the closing journal entry ->prepare the closing trial balance. Accrual accounting a system of accounting that measures the economic performance of an entity rather than just its cash flows. Under the accrual system, revenue is recognized when it is earned and expenses matched to revenue, regardless of when the cash is received or spent. Provides more relevant information to stakeholders than cash accounting. Exchange of cash is not the critical event to trigger accounting.