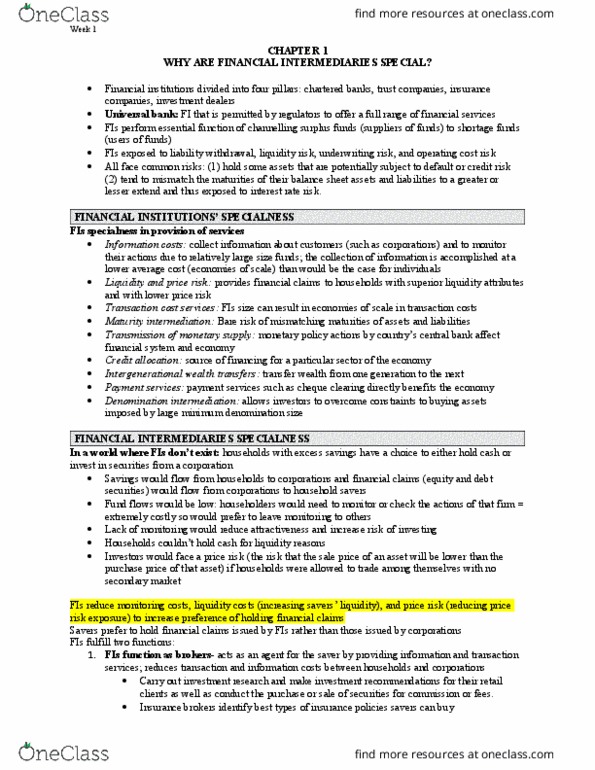

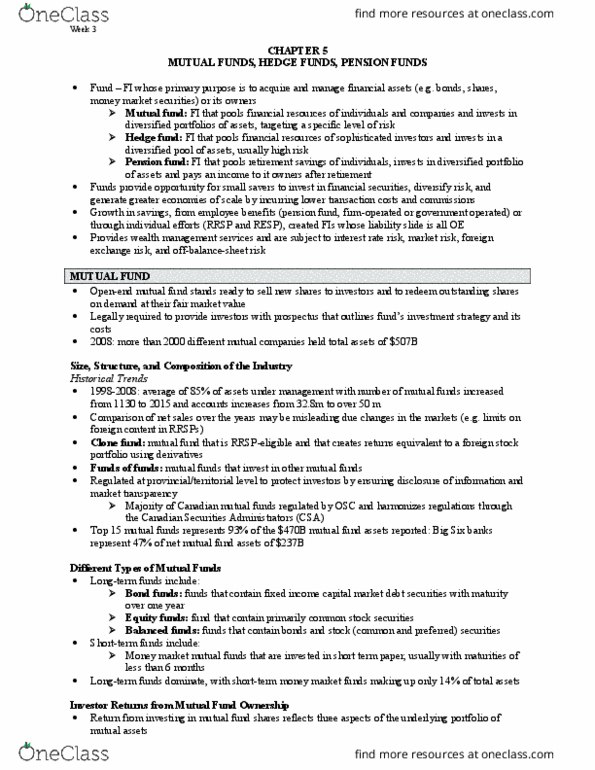

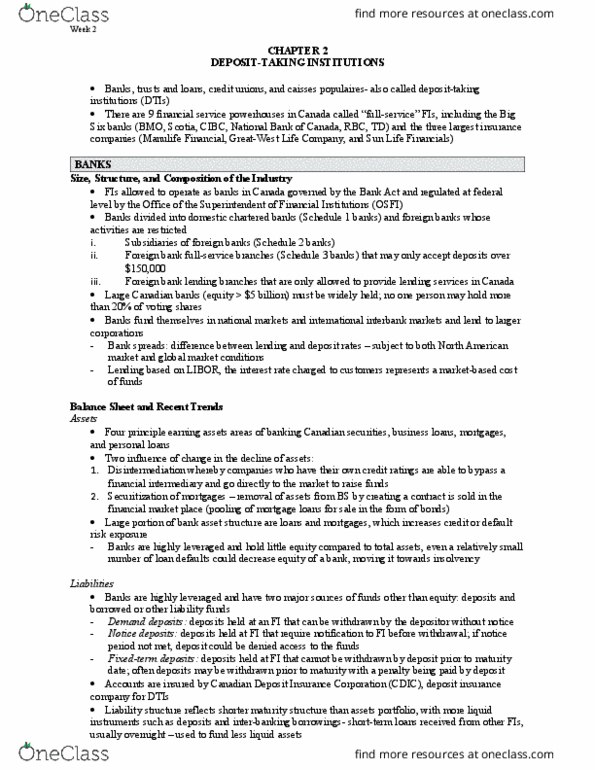

AFF 704 Chapter Notes - Chapter 9: Interest Rate Risk

65 views2 pages

1 Jun 2017

School

Department

Course

Professor

Document Summary

The duration gap model: considers market values and the maturity distributions of an fi"s assets and liabilities. Duration more complete measure of interest rate sensitivity than maturity because duration takes into account the time of arrival or payment of all cash flows as well as asset/liability"s maturity. Example: consider a loan with a 15% interest rate and required repayment of half the in principal at the end of 6 months and the other half at the end of the year. The loan is financed with a one-year gic paying 15% interest per year. Cf1/2 = . 50 [ + ( x x 15%)] pv1/2 = . 50/(1. 075) = . 49. Cf1 = [ + ( x x 15%)] pv1 = . 75/(1. 075)2 = . 51. Cf1/2 + cf1 = . 25 pv1/2 + pv1 = . Present values of the cash flows from the loan. Year x1/2 = [pv1/2]/[pv1/2 + pv1] = [. 49/100] = 0. 5349 = 53. 49%

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers