FIN 401 Chapter 16: FIN401 - Chapter 16 Textbook Notes Part 2

Document Summary

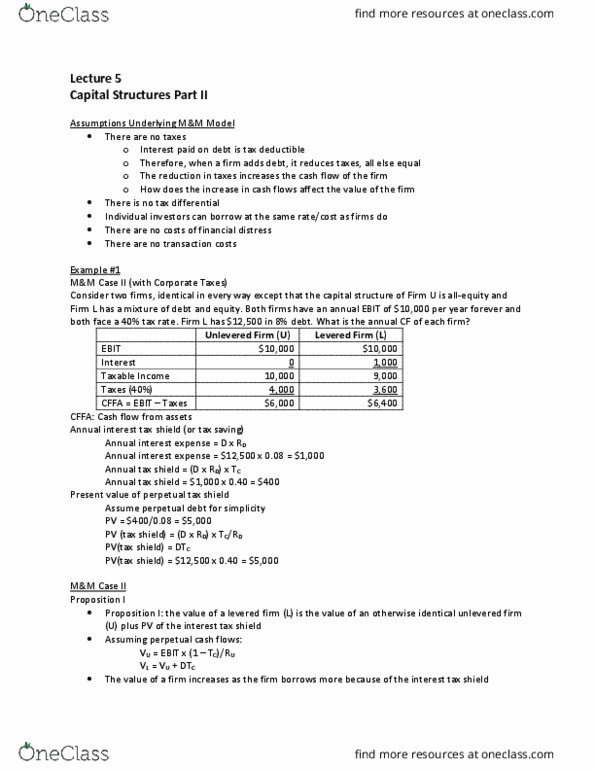

For our two firms, u and l, we can now calculate the following: to simplify things, we assume depreciation is equal to zero, we also assume capital spending is zero and there are no additions to nwc. I(cid:374) this (cid:272)ase, the (cid:272)ash flo(cid:449) f(cid:396)o(cid:373) assets is si(cid:373)pl(cid:455) e(cid:395)ual to ebit ta(cid:454)es. Since the debt is perpetual, the same shield would be generated every year forever: the after-tax cash flow to l would thus be the same that u earns plus the tax shield. In other words, the npv per dollar in debt is $. 30. I(cid:374)(cid:272)e the de(cid:271)t is (cid:449)o(cid:396)th ,(cid:1004)(cid:1004)(cid:1004), the e(cid:395)uit(cid:455) (cid:373)ust (cid:271)e (cid:449)o(cid:396)th ,3(cid:1004)(cid:1004) (cid:1005),(cid:1004)(cid:1004)(cid:1004) = ,3(cid:1004)(cid:1004). For firm l, the cost of equity is thus: the weighted average cost of capital is, without debt, the wacc is 10 percent; with debt, it is 9. 6 percent, therefore, the firm is better off with debt.