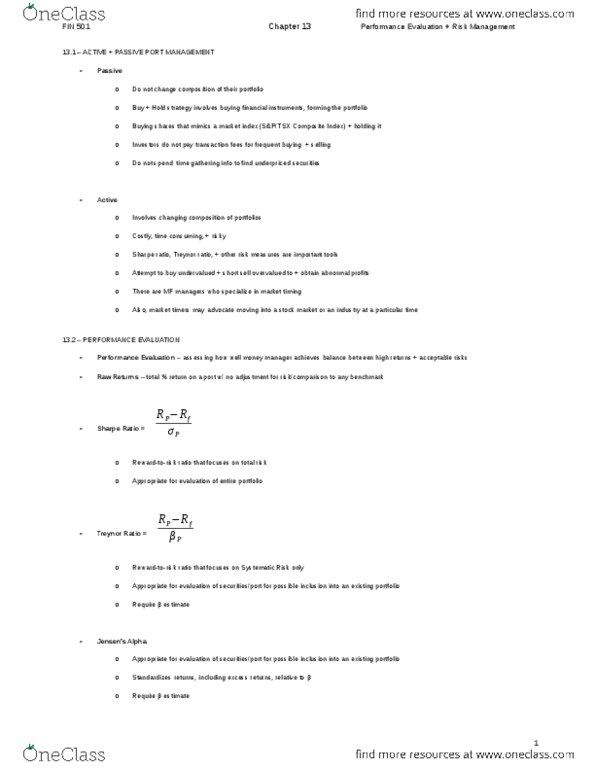

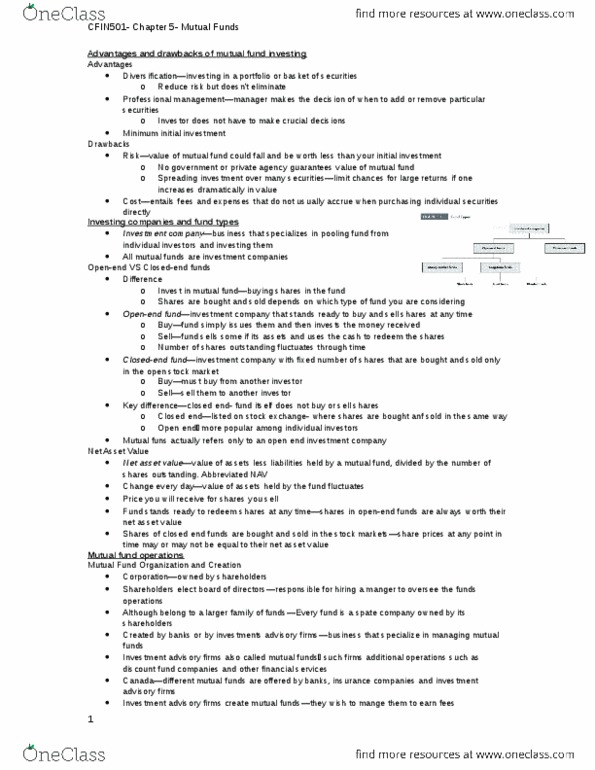

FIN 501 Chapter Notes - Chapter 13: Sharpe Ratio, Mutual Fund, Standard Deviation

Document Summary

Get access

Related Documents

Related Questions

Question 18

1. Which of the following does an efficient portfolio do?

1. Maximizes risk for a given return.

2. Minimizes risk for a given return.

3. Maximizes return for a given level of risk.

4. Minimizes return for a given level of risk.

| a. | 1 and 3. | |

| b. | 1 and 4. | |

| c. | 2 and 3. | |

| d. | 2 and 4. |

3 points

Question 19

1. The security market line does not:

| a. | Indicate the relationship between risk and return. | |

| b. | Relate the market return and beta to a stock's return. | |

| c. | Identify the optimal portfolio for the investor. | |

| d. | Use beta coefficients as a measure of risk. |

3 points

Question 20

1. Mutual funds ____ realized capital gains and income (for example, dividends received):

| a. | Retain. | |

| b. | Reinvest. | |

| c. | Distribute. | |

| d. | Distribute or reinvest. |

2 points

Question 21

1. An index fund limits its portfolio to:

| a. | High quality securities. | |

| b. | Stocks that respond to changes in the consumer price index. | |

| c. | Stocks included in an aggregate measure of stock prices. | |

| d. | Stocks of firms in a particular industry. |

2 points

Question 22

1. Mutual funds with beta coefficients greater than 1.0:

| a. | Have outperformed the market. | |

| b. | Have underperformed the market. | |

| c. | Have more systematic risk than the market. | |

| d. | Have less systematic risk than the market. |

3 points

Question 23

1. Which of the following will tend to cause a stock's price to fall?

1. The firms beta declines.

2. The firms beta increases.

3. The risk-free rate declines.

4. The risk-free rate increases.

| a. | 1 and 3. | |

| b. | 1 and 4. | |

| c. | 2 and 3. | |

| d. | 2 and 4. |

2 points

Question 24

1. The use of P/E ratios to select stocks suggests that:

| a. | High P/E stocks should be purchased. | |

| b. | Low P/E ratio stocks are overvalued. | |

| c. | A stock should be purchased if it is selling near its historic low P/E. | |

| d. | A stock should be purchased if it is selling near its historic high P/E. |

2 points

Question 25

1. What does the efficient market hypothesis require?

1. Financial markets to be competitive.

2. Prices to adjust rapidly.

3. Prices of undervalued securities to fall.

| a. | 1 and 2. | |

| b. | 1 and 3. | |

| c. | 2 and 3. | |

| d. | All of these choices. |

3 points

Question 26

1. Which of the following does the strong form of the efficient market hypothesis suggest?

1. Inside information will not lead to superior investment results.

2. Inside information will lead to superior investment results.

3. Studying financial statements will not lead to superior investment results.

4. Studying financial statements will lead to superior investment results.

| a. | 1 and 3. | |

| b. | 1 and 4. | |

| c. | 2 and 3. | |

| d. | 2 and 4. |

3 points

Question 27

1. Which of the following is the least broad-based measure of stock prices?

| a. | NASDAQ market index. | |

| b. | Dow Jones industrial average. | |

| c. | S&P 500 stock index. | |

| d. | AMEX market value index. |

3 points

Question 28

1. What is dollar-cost averaging?

| a. | Periodically buying a round lot of stock. | |

| b. | Periodically investing a specified dollar amount in a stock. | |

| c. | A means to increase the average cost basis. | |

| d. | A means to ensure a positive return. |

2 points

Question 29

1. Stock dividends cause:

| a. | The price of a share of stock to rise. | |

| b. | The price of a share of stock to fall. | |

| c. | The value of the firm to rise. | |

| d. | The value of the firm to fall. |

2 points

Question 30

1. Which of the following occurs when a stock has a two-for-one split?

| a. | The price of the stock doubles. | |

| b. | The firm's assets increase. | |

| c. | The firm's liabilities decrease. | |

| d. | The par value of the stock is reduced. |

3 points

Question 31

1. Dividend reinvestment plans offer which of the following advantages?

1. Deferment of federal income taxes.

2. A convenient means to accumulate shares.

3. Dollar-cost averaging.

| a. | 1 and 2. | |

| b. | 1 and 3. | |

| c. | 2 and 3. | |

| d. | 2. |

3 points

Question 32

1. When the Federal Reserve seeks to expand the money supply, it:

| a. | Sells securities. | |

| b. | Buy securities. | |

| c. | Runs a deficit. | |

| d. | Runs a surplus. |

2 points

Question 33

1. The sum of cash, currency, and demand deposits is:

| a. | M1. | |

| b. | M2. | |

| c. | M3. | |

| d. | M4. |

3 points

Question 34

1. If the Federal Reserve lowers the target federal funds rate:

| a. | The discount rate rises. | |

| b. | Liquidity in the banking system is increased. | |

| c. | Security prices fall. | |

| d. | Required reserves are also decreased. |

3 points

Question 35

1. The anticipation of inflation suggests that the investor should:

| a. | Buy bonds. | |

| b. | Anticipate higher interest rates. | |

| c. | Avoid real estate investments. | |

| d. | Sell stocks of gold companies. |

3 points

Question 36

1. The current ratio is unaffected by:

| a. | Using cash to pay a dividend. | |

| b. | The collection of an account receivable. | |

| c. | Selling inventory for a profit. | |

| d. | Selling bonds and using the funds to finance inventory. |

2 points

Question 37

1. Which of the following are true as the debt ratio increases?

1. Fewer assets are debt financed.

2. More assets are debt financed.

3. The ratio of debt equity increases.

4. The ratio of debt equity decreases.

| a. | 1 and 3. | |

| b. | 1 and 4. | |

| c. | 2 and 3. | |

| d. | 2 and 4. |

2 points

Question 38

1. The technical approach suggests that future stock prices are forecasted by:

| a. | Past stock rates. | |

| b. | Financial ratios. | |

| c. | Accounting statements. | |

| d. | Monetary policy. |

2 points

Question 39

1. The Dogs of the Dow strategy:

| a. | Forecasts the direction of the Dow Jones averages. | |

| b. | Suggests buying the Dow stocks with the highest dividend yields. | |

| c. | Outperforms the S&P 500. | |

| d. | Suggests buying the lowest-priced Dow stocks. |

3 points

Question 40

1. Behavioral finance combines aspects from which two fields in an attempt to identify human traits that affect investment decisions?

| a. | Accounting and finance. | |

| b. | Finance and psychology. | |

| c. | Physics and finance. | |

| d. | Finance and marketing. |

International Research Journal of Applied Finance ISSN 2229 â 6891

Vol. VI Issue â 8 August, 2015 Case Study Series

A Stock Valuation Case: An Application of the âMethod of Comparablesâ for Macyâs Shares

Halil D. Kaya* ,Julia S. Kwok

Abstract

The primary focus of this case is the application of the âMethod of Comparablesâ in the estimation of the value of a security. An investment decision will be made based on the comparison of the selling price and the estimated value. A security will be good for purchase if the estimated value is higher than the market price. This method utilizes basic financial ratios that are commonly provided by financial web sites. First, using Yahoo Finance website, the pricing, sales, book value of equity and shares outstanding data are collected for both the target firm and the competitor firms. Then, the pricing multiples (i.e. price earnings ratio, price to sales ratio and price to book ratio) of the competitors are calculated. After that, those multiples along with the target firmâs earnings, sales, book value and shares outstanding data are used to estimate target firmâs share value. The case also examines the impact of treating ânegativesâ in the data. Students will learn that replacing negative earnings with zeros tend to induce less bias in target firmâs value estimation than excluding the ânegativeâ data altogether.

Introduction

March 14, 2015 was a sunny day. Mary took advantage of the nice weather to have lunch at the Mall. On her way back to work, she walked by Susanâs investment office. Susan was Maryâs college roommate. They both liked shopping together to find new fashionable clothes. Looking at her watch, Mary realized she had half an hour to spend. She thought she would drop by and say hello to Susan.

The Performance of Macyâs

âHi, Susan, how are you?â How is your business?â said Mary. Susan was a recent finance graduate. Susan replied, âI am doing fine. Thank you. After so many years, the market is still recovering from the mortgage crisis; many investors have been buying back stocks that they have sold during the crisis. What are you up to?â âI want to start my investment in securities, too. I have a couple thousand dollars, would Macyâs be a good stock to invest in now? That was our favorite store to shop among all of the department stores,â Mary exclaimed. She added, âAlso, I read from Motleyâs Foolâs article on Macyâs today about its earnings per share growth for the last 16 quartersâ (Zahid Waheed, 2014).

In response to Maryâs questions, Susan checked the monthly adjusted returns of Macyâs in Yahoo Finance. She found that, since March 2010, Macyâs stock price had an average annual increase of 23.5% over the last 5 years. The stock rose from $19.98 to $57.38. Susan then told Mary that Macyâs was indeed a growing stock. She added that its success could be attributed to the omni-channel integration, e-commerce and magic selling strategies which allowed merging of sales channels, online shopping and better customer care. Since investment strategy 101 is to buy low, and sell high, given Macyâs stock price had been going up, Susan was not sure whether Macyâs was currently overvalued or undervalued by the market.

The Method of Comparables

Susan remembered her class lecture on the two types of valuation of stocks, namely absolute and relative evaluation. The absolute evaluation focuses on finding the intrinsic value of the security based on fundamentals. That involves more complicated models of discounting cash flows from dividends, operations and residual income.

On the other hand, relative evaluation is quick and easy to use. It assumes two similar securities should sell for one price in an efficient market, i.e. âLaw of One Price.â So an analyst can estimate its stock price by multiplying target companyâs specific earnings, sales and equity value data by the earning, sales and equity âper shareâ financial multiples of its competitors.

Since Mary was not familiarized with financial models, Susan decided to use the easy-toperform-and-analyze âComparables Methodâ to estimate the relative value of Macyâs stock.

The Financial Data

Dillards, JC Penney and Nordstrom were selected as competitors of Macyâs as they were all in retail department store business. Susan would need some financial data regarding these companies. She went to SECâs (i.e. Securities and Exchange Commission) website and downloaded these companiesâ most recent balance sheet and income statement data. Out of those statements, she knew that she would need the EPS (i.e. earnings per share), the sales number, the number of outstanding shares, and the book value of equity. She also knew that she would need the current share price for each company. After some work, she had found all the necessary information to run the analysis. Below were the data that she had gathered:

All data are in US$ except for the number of outstanding shares. The share price as of March 15, 2014 is shown in the first column. The âEarnings per shareâ is shown in the second column. The third column reports the book value of equity. The last column shows the number of outstanding shares.

| Firm | P ($) | EPS ($) | Sales ($) | BV of equity ($) | # of shares |

| Macy's | 58.58 | 3.93 | 27,931 mil. | 6,249 mil. | 378.3 mil. |

| Dillard's | 90.61 | 7.10 | 6,532 mil. | 1,992 mil. | 45.6 mil. |

| JC Penney | 8.71 | -5.57 | 11,859 mil. | 3,087 mil. | 249.3 mil. |

| Nordstrom | 61.33 | 3.77 | 12,166 mil. | 2,080 mil. | 194.5 mil. |

The Decision

Susan thinks that the following steps would be necessary to perform the analysis:

1.Based on the data above, calculate Sales per share, BV of equity/share values of all firms. Note that EPS is directly given.

2.Calculate P/E, P/Sales, and P/B for all of Macyâs competitors based on the data obtained.

3.Find the average of the P/E, P/Sales, and P/B multiples for the three competitors.

4.Multiply those averages calculated in step 3 with Macyâs EPS, Sales per share, and BV of equity/share values, respectively to get three value estimates for Macyâs shares.

5.The average of the three estimates would then be Susanâs best estimate of Macyâs value per share.

answer # 1-5 please