BUS 393 Chapter Notes - Chapter 11: Security Interest, Secured Creditor, Chattel Mortgage

20 Nov 2011

School

Department

Course

Professor

Document Summary

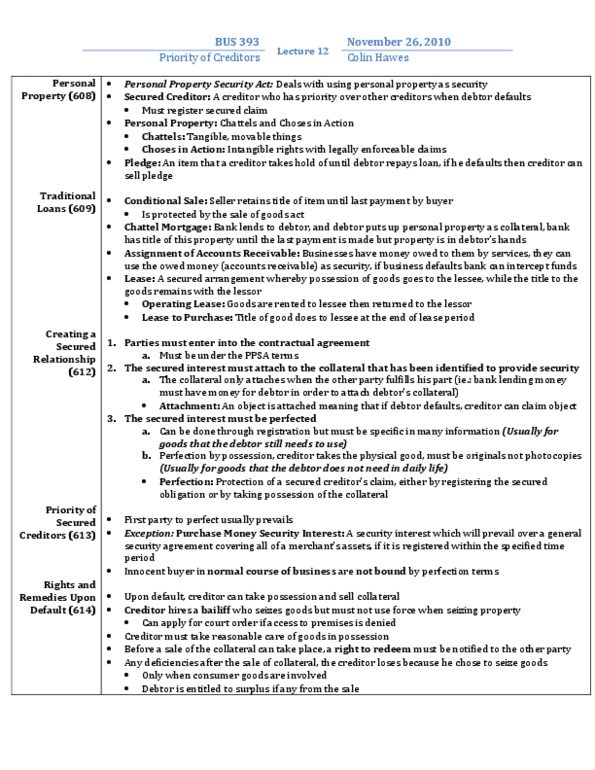

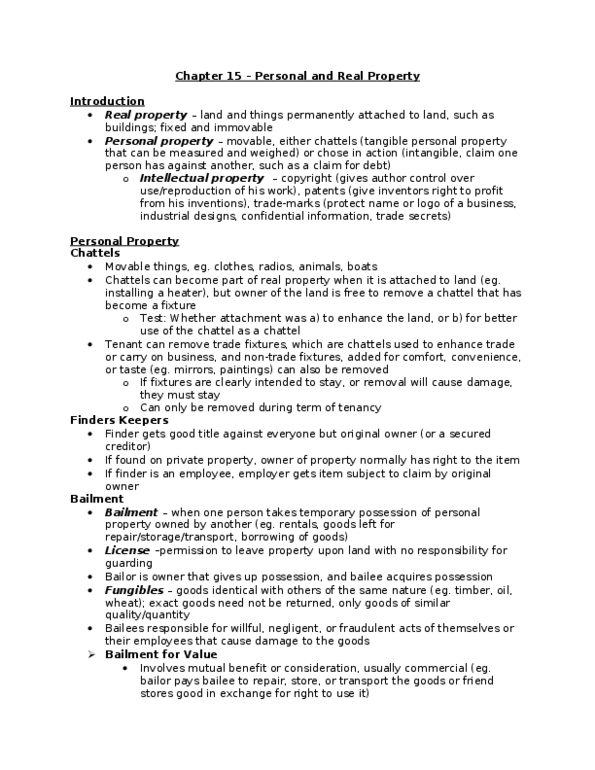

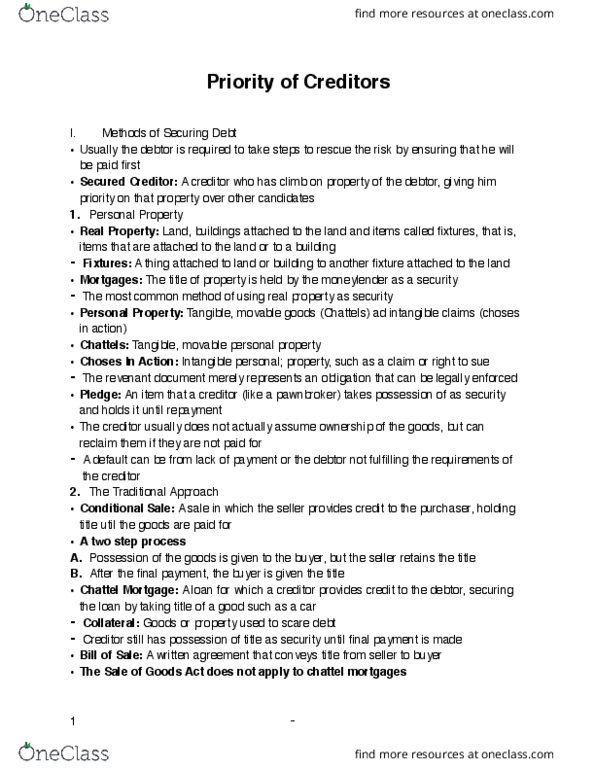

A buyer of the car would search the registry and be forewarned to avoid buying it. In the case of default, the bank can recover the vehicle, even from an innocent 3rd party. Guarantees: guarantors must pay when a debtor defaults creates a secondary or conditional obligation that arises only in the event of default. Floating charges: allows flexibility in items taken for security (eg. growing crops, inventories, goods in process of manufacture) Floating charge a security not fixed on any particular assets until default or other specified event, allows business to continue without interference, while giving creditor priority in case of default (eg. inventory, goods in process of manufacturing) In consumer transactions, third party rights as a holder in due course do not apply. Landlord has right to seize, hold, and sell tenant"s assets on rented premises to pay for rent owed (distress)