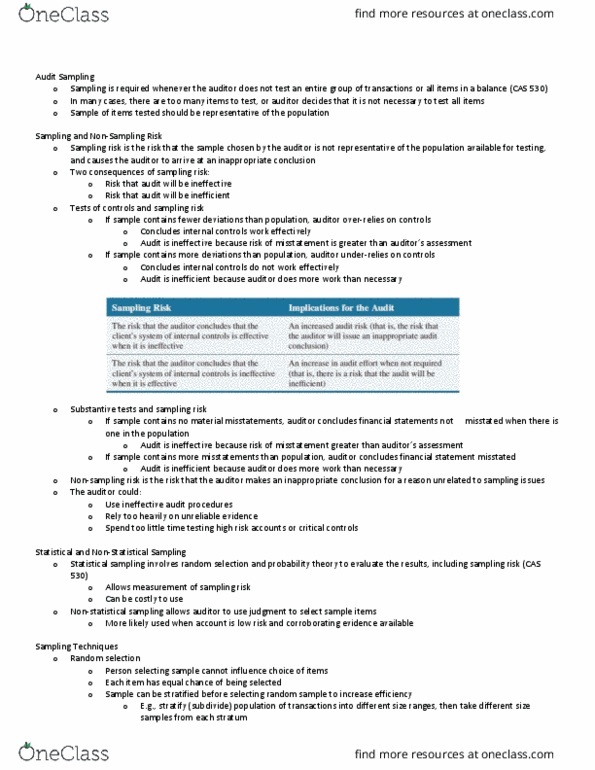

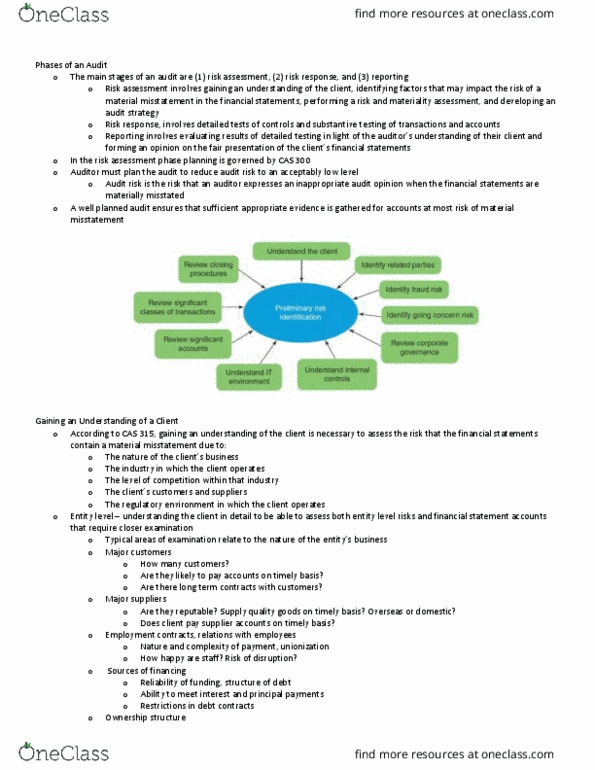

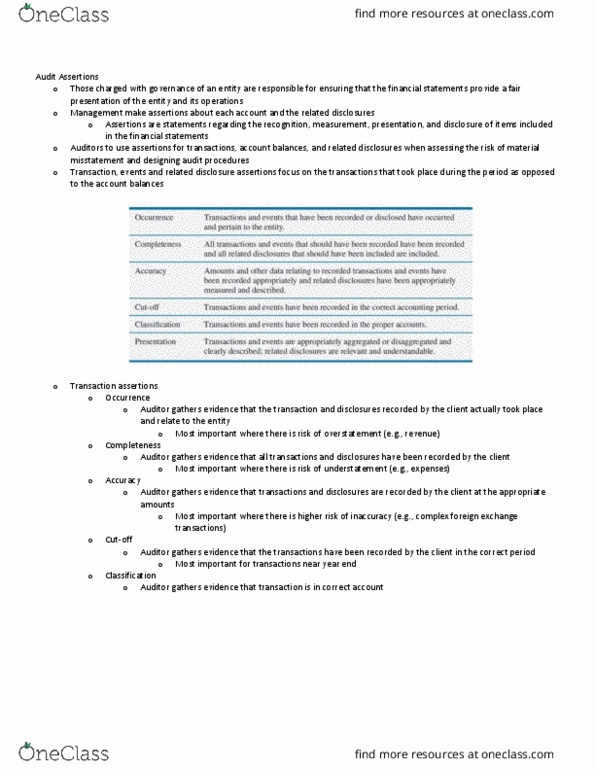

ADMN 4301H Chapter Notes - Chapter 4: Audit Risk, Financial Statement, Balance Sheet

30 Mar 2020

School

Department

Course

Professor

Document Summary

Identification of accounts and related assertions most at risk of material misstatement (inherent risk: assertions are statements made by management about recognition, measurement, presentation, and disclosure of items in the financial statements and notes. For example, all inventory items stated on balance sheet actually exist. Significant risks require special audit consideration (cas 315: risks are more significant when they involve: If ir and cr are high, auditor will set dr as low, and perform more detailed substantive procedures. If ir and cr are low, auditor will set dr as high, and reduce reliance on detailed substantive procedures. Materiality: materiality guides audit planning, testing, and assessment of information in the financial statements. Information is material if it impacts on the decision-making process of users of the financial statements. Information could be considered material because of its qualitative or quantitative characteristics: qualitative materiality factors, nature of the item, for example,