ADMN 4303H Chapter Notes - Chapter 12: Financial Statement, Fund Accounting, Buyout

30 Mar 2020

School

Department

Course

Professor

Document Summary

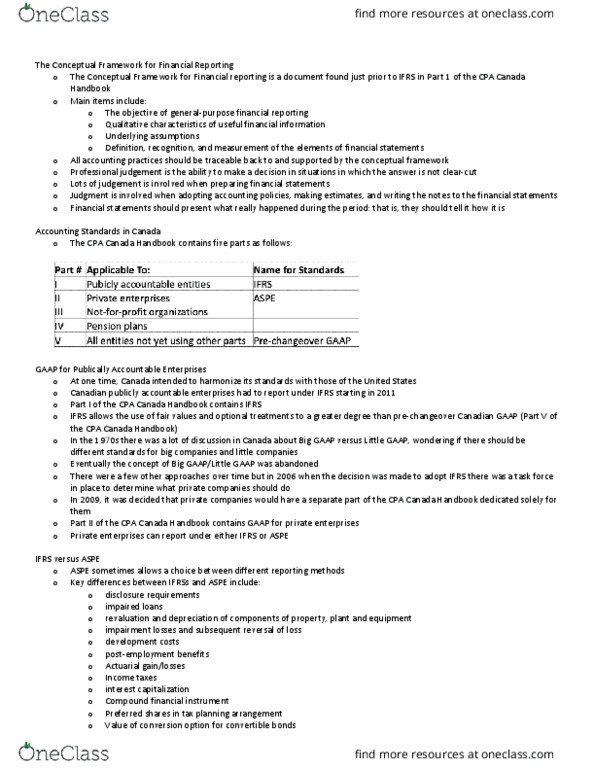

Introduction: not-for-profit organizations (nfpos) are defined in part iii of the cpa canada handbook as, entities, normally without transferable ownership interests, organized and operated exclusively for social, educational, professional, religious, health, charitable or any other not-for-profit purpose. A not-for-profit organization"s members, contributors and other resource providers do not, in such capacity, receive any financial return directly from the organization. [4400. 02: nfpos differ from profit-oriented organizations in the following ways: Section 3463 reporting employee future benefits by not-for-profit organizations: this section provides guidance for defined benefit plans on the recognition and presentation of remeasurements and other items that differs from the guidance in section 3462. Section 4400 financial statement presentation by not-for-profit organizations: an nfpo must present the following financial statements for eternal reporting purposes: Section 4431 tangible capital assets held by not-for-profit organizations. In december 2010 when part iii of the handbook was introduced, accounting for capital assets was split into two sections,