ADMN 4710H Chapter Notes - Chapter 18: Capital Gain, Double Taxation, Cash Flow

30 Mar 2020

School

Department

Course

Professor

Document Summary

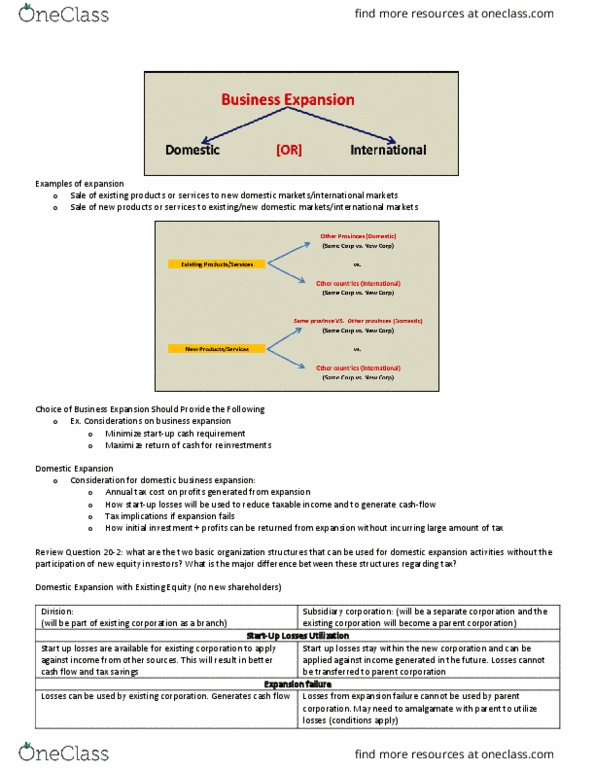

Mr. x wants to sell the x-corp (shares or assets: after the sale of assets by x-corporation, true proceeds for x-corporation: selling price less taxes paid (or payable) Cca: this is an added benefit for y-corporation, therefore, purchase of assets is more attractive for y-corporation. Review question 18-2: types of gains or losses may occur for tax purposes when specific business assets are sold. Types of gains/losses that occur when specific business assets are sold: Note: a/r: with out without section 22 election. Taxable capital gains/recapture/terminal loss (no capital losses from depreciable properties) Any loss will be treated as capital loss. Any loss will be treated as business loss (50% deductible) (100% deductible) Components of distribution to shareholder from wind-up of corporation: puc, capital dividend, taxable dividend. Wind up of corporation means dissolving the corporation: examples. Sell all assets: pay off creditors, distribute any remaining assets (cash) to shareholders, close down the corporation.