ACCTG322 Chapter Notes - Chapter 7: Contribution Margin, Operating Leverage, Budget

8 Apr 2014

School

Department

Course

Professor

Document Summary

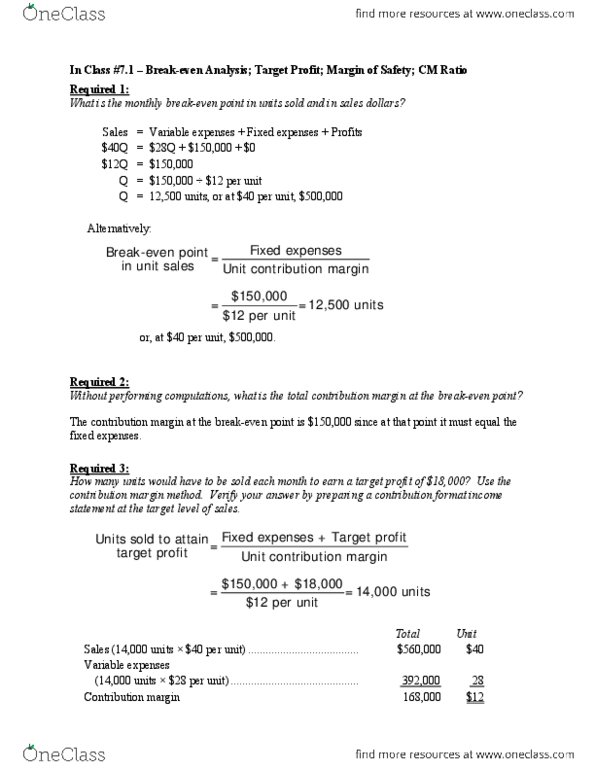

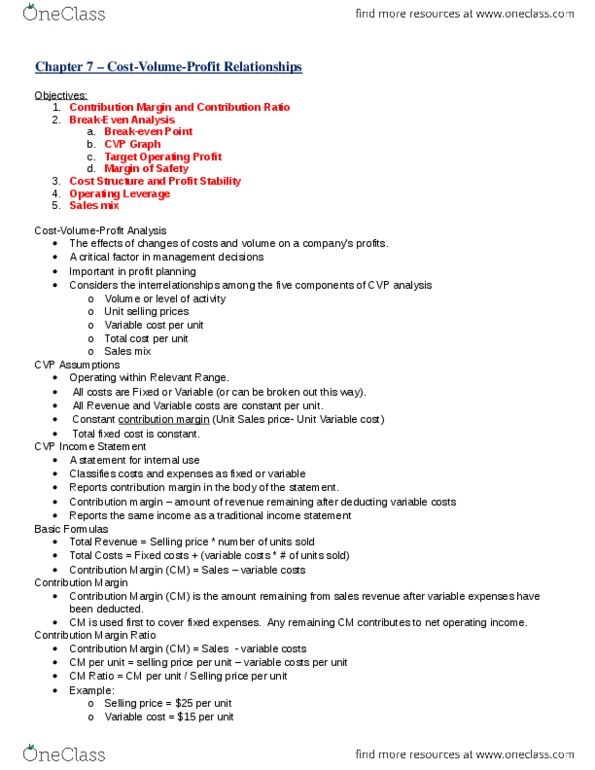

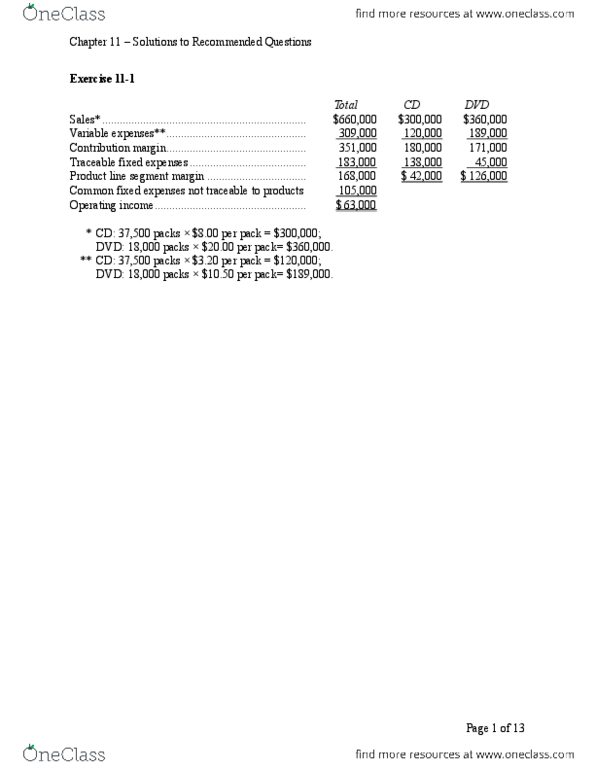

Problem 7-18: the cm ratio is 60%: =,000 sales: ,000 increased sales 60% cm ratio = ,000 increased contribution margin. Since fixed costs will not change, operating income should also increase by ,000. 4 16% = 64% increase in operating income. In dollars, this increase would be 64% . * 23,000 units 1. 3 = 29,900 units. ** per unit (1 0. 12) = . 40 per unit. No, the changes should not be made since operating income decreases. Chapter 7 solutions to recommended questions: expected total contribution margin: 23,000 units 150% per unit* Incremental contribution margin, and the amount by which advertising can be increased with operating income remaining unchanged *,000 ,000 = 43%: break-even sales: 20: memo to the president: although the company met its sales budget of ,000 for the month, the mix of products sold changed substantially from that budgeted.