AFM101 Chapter Notes - Chapter 7: Book Value

10 Jun 2018

School

Department

Course

Professor

AFSA Education

Bad debts will likely increase as well customers will likely default on

their payments (write-off of trade receivables).

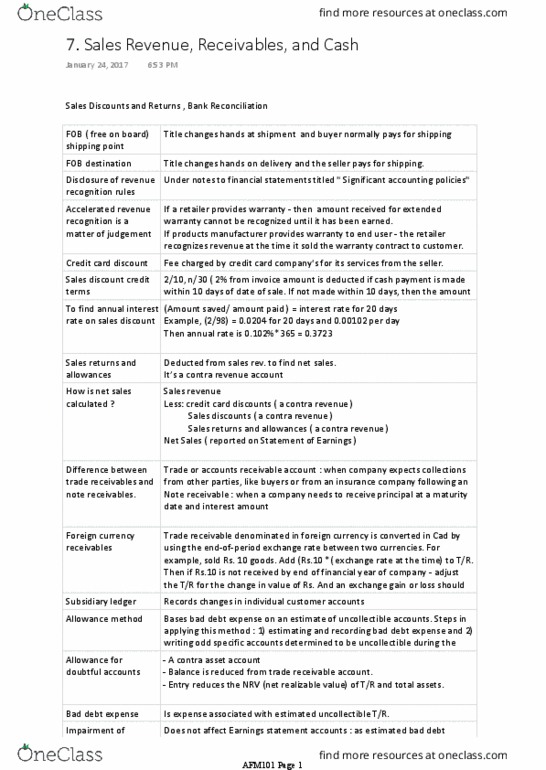

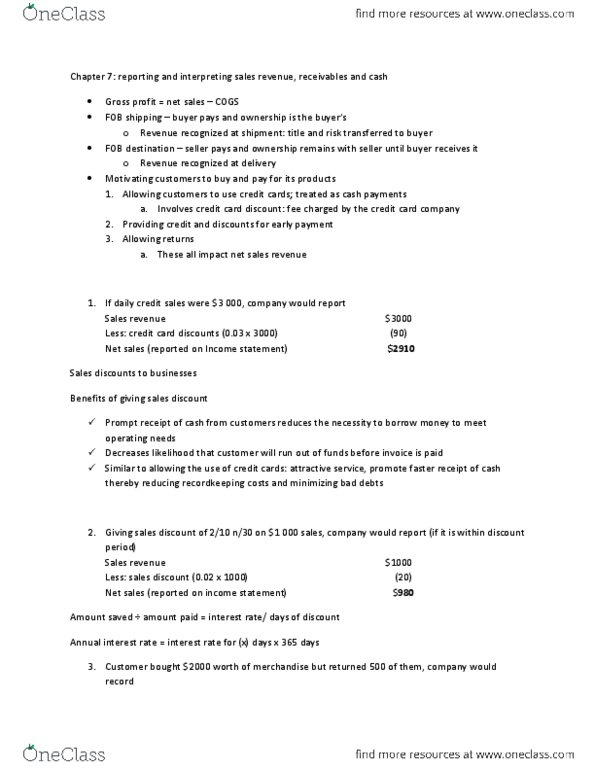

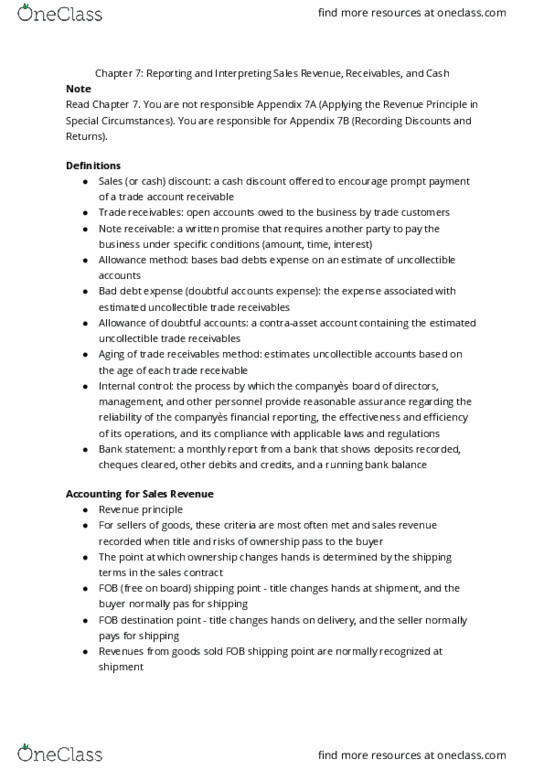

- SUBSIDIARY LEDGER: Separate accounts for each of the retailers and wholesalers.

o Detailed amounts of trade receivables on the Statement of Financial Position.

- Allowance Method = Bases bad debt expense on an estimate of uncollectible accounts.

- 2 primary step in applying this method:

1. Estimating and recording bad debt expense.

2. Writing off specific accounts determined to be uncollectible during the period.

Various transactions that affected the Allowance for Doubtful Accounts:

1. Recording Bad Debt Expense Estimates.

Definitions:

(a) Bad Debt Expense = expense associated with estimated uncollectible trade

receivables.

Some companies include this Expense in the General & Admin. Expense on

the Statement of Earnings.

Bad Debt Expense decreases Net Earnings & Shareholders’ Equity.

(b) Allowance for Doubtful Accounts = a contra-asset account containing the

estimated uncollectible trade receivables.

Ending Balance = Beginning Balance + Bad Debt Expenses – Write-offs

JOURNAL ENTRY:

DR: Bad debt expense (E)

CR: Allowance for doubtful accounts (contra-asset) (XA)

2. Impaired Receivables – Writing Off Specific Uncollectible Accounts.

This will occur once it is determined that a customer will not pay its debts

(example: due to bankruptcy); receivable is considered IMPAIRED.

Does NOT affect the Statement of Earnings accounts. The estimated Bad Debt

Expense was already recorded with an adjusting entry in the period of sale. The entry

did not change carrying amount of trade receivables decrease in assets account

(TR) was offset by an equal decrease in the contra-asset account (AfDA).

JOURNAL ENTRY:

DR: Allowance for doubtful accounts (XA)

CR: Trade receivables (A)

3. Recovery of Accounts Previously Written Off.

When customer makes payment on an account previously written off, the initial

journal entry to write off the account is REVERSED for the amount that is collected.

Another journal entry is made to record the collection of cash.

Note: net effect on the amount of Trade Receivables is zero.

JOURNAL ENTRY:

DR: Trade receivables (A)

CR: Allowance for doubtful accounts (XA)

DR: Cash (A)

CR: Trade receivables (A)

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Bad debts will likely increase as well customers will likely default on their payments (write-off of trade receivables). Subsidiary ledger: separate accounts for each of the retailers and wholesalers: detailed amounts of trade receivables on the statement of financial position. Allowance method = bases bad debt expense on an estimate of uncollectible accounts. 2 primary step in applying this method: estimating and recording bad debt expense, writing off specific accounts determined to be uncollectible during the period. Various transactions that affected the allowance for doubtful accounts: recording bad debt expense estimates. Definitions: (a) bad debt expense = expense associated with estimated uncollectible trade receivables. Some companies include this expense in the general & admin. Bad debt expense decreases net earnings & shareholders" equity. (b) allowance for doubtful accounts = a contra-asset account containing the estimated uncollectible trade receivables. Ending balance = beginning balance + bad debt expenses write-offs.