AFM291 Chapter Notes - Chapter 7: Discounted Cash Flow, Earnings Management, Retained Earnings

26 Jun 2018

School

Department

Course

Professor

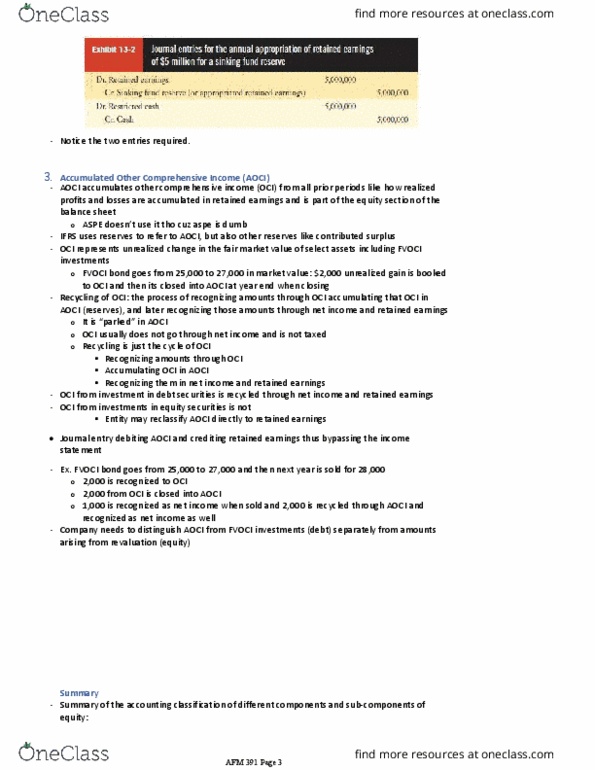

When the entity sells investments measured at FVOCI, the total gain or loss flows through

income.

The differences in treatment between FVPL and FVOCI applies only to unrealized gains and

losses. Realized gains and losses from actual disposals of financial assets flow through net

income and not OCI. Thus, OCI is recycled into net income.

3. Amortized Cost

A category of financial investments that have fixed or determinable payments representing

principal and interest and the entity intends to collect theses contractual cash flows

Applies only to debt investments

Implementation of amortized cost method requires discounted cash flow analysis

4. Exception for Equity Investments with an Irrevocable Election

IFRS 9 provides an exception where equity investments that will be otherwise be treated as

FVPL, a firm can elect to present changes in the fair value of an investment through OCI

Conditions that must be met to treat equity through OCI

o Must be made when the entity initially acquires the investment

o The investment must be in equity

o The election is irrevocable, meaning that the investment cannot be reclassified into

another category

While the entity holds the investment, any dividends received would be recorded in net income

while changes in fair value flow through OCI, just like for FVOCI discussed above.

The only difference is, upon sale/de-recognition, any gains/losses does not flow through net

income, but continues to go into OCI and the accumulated other comprehensive income (AOCI)

for the investment would be directly transferred to retained earnings. No recycling here.

See exhibit on 306 and the following paragraph.

Why does IFRS 9 prevents the recycling of OCI generated by investments? – Answer: due to

earnings management

o If the standards specified recycling of OCI, then management can pick the opportune

time to sell financial assets with this election in order to transfer unrealized gains (or

losses) out of AOCI and into gains/loss to boost (or reduce) net income

o Without recycling, all of the accumulated gains/losses bypass the income statement and

transfer directly into retained earnings, precluding the earnings management

5. Reclassification from one category to another

How to classify financial assets depends on the business model selected by management rather

than the characteristics inherent in the investments

If there are no constraints on the ability of managing to reclassify, then there would be

significant opportunities from companies to manage earnings such as transferring unrealized

gains from FVOCI to FVPL and transferring unrealized losses from FVPL to FVOCI. (recognizing

unrealized gains and deferring losses)

IFRS 9 has guidelines for reclassification of financial assets

o Derivatives can only be classified as FVPL (with the exception of derivatives used in

hedging)

Document Summary

When the entity sells investments measured at fvoci, the total gain or loss flows through income. The differences in treatment between fvpl and fvoci applies only to unrealized gains and losses. Realized gains and losses from actual disposals of financial assets flow through net income and not oci. Thus, oci is recycled into net income: amortized cost. A category of financial investments that have fixed or determinable payments representing principal and interest and the entity intends to collect theses contractual cash flows. Implementation of amortized cost method requires discounted cash flow analysis: exception for equity investments with an irrevocable election. Ifrs 9 provides an exception where equity investments that will be otherwise be treated as. Fvpl, a firm can elect to present changes in the fair value of an investment through oci.